An APR calculator helps estimate the true cost of borrowing money by calculating the annual percentage rate (APR) based on interest charges and additional loan fees. Unlike a basic interest rate, APR provides a broader view of borrowing costs, making it easier to compare credit cards, personal loans, mortgages, auto loans, and other financing options.

How an APR Calculator Works

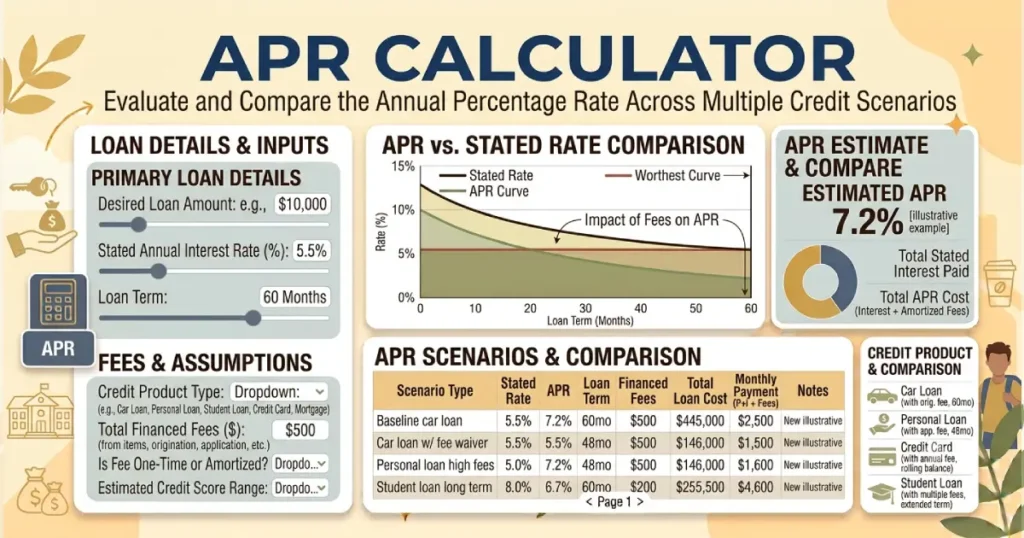

An APR calculator determines the effective annual cost of a loan by considering the interest rate along with certain fees and charges associated with borrowing. It converts these costs into a yearly percentage, allowing borrowers to compare different loan offers more accurately.

The calculation may consider:

- Loan amount

- Interest rate

- Loan term

- Origination fees

- Closing costs

- Other borrowing charges

Because APR includes more than just the stated interest rate, it is often a better measurement when comparing loans with different fee structures.

APR vs Interest Rate: What Is the Difference?

Interest rate and APR are related but not identical. The interest rate represents the cost of borrowing the principal amount, while APR includes the interest rate plus certain fees and charges.

| Feature | Interest Rate | APR |

|---|---|---|

| Includes loan interest | Yes | Yes |

| Includes certain fees | No | Usually yes |

| Used for comparing loan costs | Limited | More useful |

| Commonly shown for | All types of loans | Mortgages, personal loans, credit products |

For example, two lenders may advertise the same interest rate, but the lender charging higher fees may have a higher APR.

What Information Do You Need?

| Input | Description |

|---|---|

| Loan amount | The amount borrowed from the lender. |

| Interest rate | The stated annual rate charged on the loan. |

| Loan term | The length of time you will repay the loan. |

| Fees | Additional borrowing costs included in the APR calculation. |

| Payment frequency | How often payments are made. |

Why Use an APR Calculator?

Looking only at the advertised interest rate can make one loan appear cheaper than another. An APR calculator provides a more complete estimate of the total borrowing cost.

Borrowers commonly use APR calculations to:

- Compare loan offers from different lenders.

- Understand the cost of financing.

- Estimate the impact of fees.

- Evaluate credit card borrowing costs.

- Compare mortgage options.

- Make more informed borrowing decisions.

APR Calculation Example

Suppose you borrow $20,000 for a personal loan. One lender offers a lower interest rate but charges higher upfront fees, while another lender charges a slightly higher rate with fewer fees.

The APR may show that the loan with the lower advertised rate is not necessarily the cheaper option after fees are included.

| Loan Feature | Example |

|---|---|

| Loan amount | $20,000 |

| Interest rate | 8% |

| Loan term | 5 years |

| Additional fees | $500 |

The APR calculation combines these costs into one annual percentage figure.

Types of Loans Where APR Matters

Mortgage APR

Mortgage APR helps home buyers compare the total cost of mortgage offers because it may include lender fees, points, and certain closing costs.

Personal Loan APR

For personal loans, APR helps borrowers compare offers that may have different origination fees, repayment terms, and interest rates.

Credit Card APR

Credit cards often advertise APR as the yearly cost of carrying a balance. A higher APR generally results in higher interest charges when balances are not paid in full.

Auto Loan APR

Auto loan APR allows buyers to compare financing options by considering the interest rate and certain loan costs.

Factors That Affect Your APR

Credit Score

Your credit score is one of the biggest factors affecting the APR you receive. Borrowers with stronger credit histories often qualify for lower rates.

Loan Amount

The amount borrowed can influence available loan terms and overall borrowing costs.

Loan Term

Longer repayment periods may reduce monthly payments but can increase the total amount of interest paid.

Fees

Origination fees, closing costs, and other charges can increase APR because they increase the overall cost of borrowing.

Market Conditions

Interest rates can change based on broader economic conditions and lender policies.

APR vs APY: What Is the Difference?

APR and APY are often confused because both describe annual percentages, but they measure different things.

| Term | Meaning |

|---|---|

| APR | Annual cost of borrowing, including interest and certain fees. |

| APY | Annual yield that includes the effect of compound interest, commonly used for savings. |

APR is generally used when discussing loans, while APY is commonly used when discussing deposit accounts and investments.

Common APR Mistakes

- Comparing loans using only the interest rate.

- Ignoring fees included in the loan agreement.

- Choosing a loan based only on monthly payment.

- Not considering the total repayment cost.

- Assuming the lowest advertised rate is always the cheapest option.

How to Get a Lower APR

- Improve your credit score before applying.

- Compare offers from multiple lenders.

- Reduce existing debt when possible.

- Choose a shorter loan term if affordable.

- Review all fees before accepting financing.

A lower APR can significantly reduce borrowing costs, especially for large loans or long repayment periods.

Frequently Asked Questions

An APR calculator estimates the annual percentage rate of a loan by considering the interest rate and certain fees. It helps borrowers understand the true cost of borrowing and compare different financing options.

APR is calculated by combining the loan interest cost with certain fees and charges, then expressing the total borrowing cost as an annual percentage rate.

The interest rate only shows the cost of borrowing the principal amount. APR includes the interest rate plus certain fees, making it a more complete measure of loan costs.

APR is often higher because it may include fees and additional borrowing costs that are not included in the stated interest rate.

A lower APR usually means lower borrowing costs, but borrowers should also consider loan terms, monthly payments, fees, and repayment flexibility before choosing a loan.

A higher APR generally increases monthly payments because you pay more interest over the repayment period. A lower APR can reduce both monthly costs and total interest paid.

A good APR depends on the loan type, market conditions, credit score, and borrower profile. Comparing multiple offers is the best way to find competitive financing.

APR includes many borrowing costs, but the exact fees included depend on the type of loan and applicable regulations. Always review the loan agreement for complete details.