A credit card payoff calculator helps you estimate how long it will take to pay off credit card debt, how much interest you may pay, and how increasing your monthly payments can help you become debt-free faster. By entering your current balance, interest rate, and payment amount, you can create a clearer repayment plan and understand the true cost of carrying credit card debt.

How a Credit Card Payoff Calculator Works

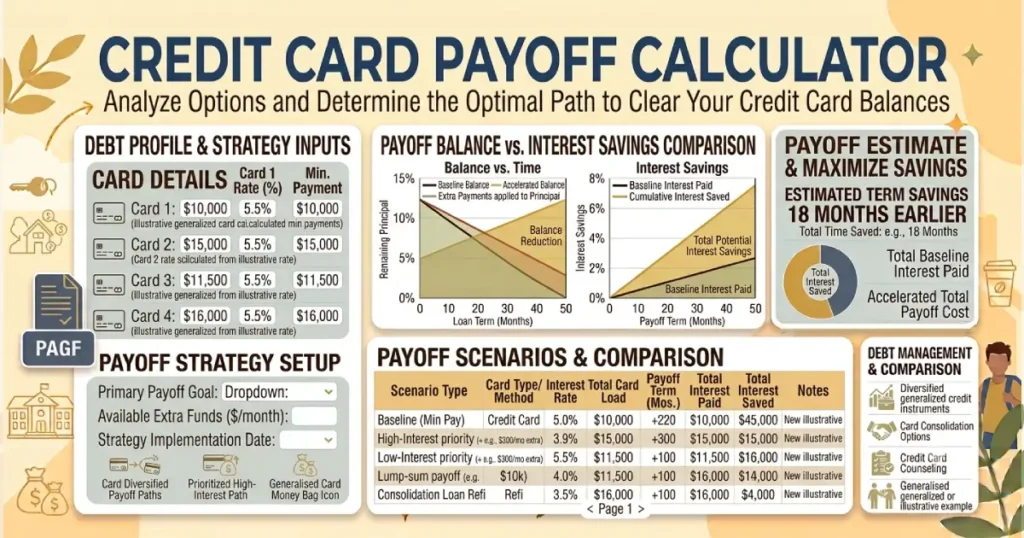

A credit card payoff calculator estimates your repayment timeline based on your outstanding balance, annual percentage rate (APR), and monthly payment. Credit cards typically use revolving credit, meaning the balance can continue growing if new purchases are added or payments are too small to cover interest and principal.

The calculator can show:

- Credit card payoff time

- Monthly payment needed to pay off credit cards

- Total interest paid

- How much you can save by paying extra

- Estimated debt-free date

The results are estimates because actual credit card interest calculations depend on the card issuer, daily balances, payment timing, fees, and new charges.

What Information Do You Need?

| Input | Description |

|---|---|

| Current balance | The total amount you currently owe on your credit card. |

| Interest rate (APR) | The annual percentage rate charged on unpaid balances. |

| Monthly payment | The amount you plan to pay each month. |

| Additional monthly payment | Extra money added to reduce the balance faster. |

| New monthly charges | Any additional purchases added while repaying the debt. |

How Credit Card Payoff Is Calculated

Credit card repayment depends on the relationship between your balance, interest rate, and payment amount. Each month, interest is added to your balance, and your payment reduces the remaining amount.

If your monthly payment is only slightly higher than the interest charged, your balance may decrease very slowly. Increasing your payment can significantly reduce both the repayment period and total interest cost.

| Payment Strategy | Effect |

|---|---|

| Minimum payment only | Usually takes longer and costs more interest. |

| Fixed higher payment | Reduces debt faster and lowers interest costs. |

| Extra payments | Can shorten payoff time significantly. |

Understanding Credit Card APR

The credit card APR represents the yearly cost of borrowing money on your card. Unlike installment loans with fixed repayment schedules, credit card balances can continue accumulating interest as long as money remains unpaid.

A higher APR can make debt repayment much more expensive because more of each payment goes toward interest charges.

Factors that affect your credit card costs include:

- Interest rate

- Outstanding balance

- Payment amount

- Late fees

- New purchases

Why Use a Credit Card Payoff Calculator?

A calculator helps you understand the impact of your repayment choices before committing to a strategy.

- Find out how long it will take to pay off credit card debt.

- Estimate total interest costs.

- Compare different monthly payment amounts.

- Create a realistic debt repayment plan.

- See the benefits of paying more than the minimum.

- Plan a path toward becoming debt-free.

Seeing the numbers clearly can make it easier to choose a repayment approach that fits your budget.

Minimum Payment vs Paying More

Credit card companies typically require a minimum monthly payment. While making the minimum payment keeps the account current, it can result in a long repayment period and significantly higher interest costs.

| Approach | Advantages | Disadvantages |

|---|---|---|

| Minimum payment | Lower monthly cost | Longer repayment and more interest |

| Higher monthly payment | Faster payoff and lower interest | Requires more monthly cash flow |

| Lump-sum payment | Immediately reduces balance | Requires available savings |

Credit Card Debt Payoff Strategies

Debt Avalanche Method

The debt avalanche method focuses on paying off the credit card with the highest interest rate first while making minimum payments on other accounts. This approach can reduce the total interest paid.

Debt Snowball Method

The debt snowball method focuses on paying off the smallest balance first. Some borrowers prefer this approach because early victories can provide motivation to continue repayment.

Balance Transfer Strategy

A balance transfer may allow eligible borrowers to move debt to another card with a lower promotional interest rate. However, transfer fees and promotional periods should be carefully reviewed.

Debt Consolidation

A debt consolidation loan combines multiple debts into one payment. Depending on the interest rate and fees, it may simplify repayment or reduce borrowing costs.

Factors That Affect Credit Card Payoff Time

Balance Amount

A larger balance requires more time and money to repay, especially when combined with a high APR.

Interest Rate

Higher interest rates increase the cost of carrying debt and slow down repayment progress.

Monthly Payment

The amount you pay each month has one of the biggest effects on how quickly your balance decreases.

New Purchases

Continuing to add new charges while paying down debt can extend the repayment timeline.

Fees

Late fees and other charges can increase your balance and make repayment more difficult.

How to Pay Off Credit Card Debt Faster

- Pay more than the minimum payment whenever possible.

- Stop adding new purchases to high-interest cards.

- Prioritize cards with the highest APR.

- Automate payments to avoid missed due dates.

- Review your budget for additional repayment money.

- Consider lower-interest alternatives carefully.

A credit card payoff calculator with extra payments can help you see how small increases in monthly payments may reduce your debt timeline.

Common Credit Card Payoff Mistakes

- Only making minimum payments without understanding the cost.

- Ignoring the interest rate.

- Using credit cards while trying to repay existing debt.

- Closing accounts without considering credit score effects.

- Taking on new debt before paying down balances.

Frequently Asked Questions

A credit card payoff calculator estimates how long it will take to eliminate your balance based on your current debt, APR, and monthly payment. It also estimates the interest you may pay during repayment.

The time required depends on your balance, interest rate, and monthly payment amount. Paying more than the minimum can significantly shorten the repayment period.

The right payment depends on your budget and debt amount. A calculator can show different payment scenarios and help determine a realistic amount to reach a debt-free goal.

The right payment depends on your budget and debt amount. A calculator can show different payment scenarios and help determine a realistic amount to reach a debt-free goal.

Yes. Paying more than the minimum reduces the balance faster, which can lower the amount of interest charged over time.

The fastest approach usually involves increasing monthly payments, avoiding new charges, and focusing repayment on high-interest balances.

Some calculators allow multiple balances and interest rates to be entered. This can help compare repayment strategies across several credit card accounts.

Debt snowball focuses on paying the smallest balance first, while debt avalanche focuses on the highest interest rate first. Both methods can help organize repayment.

Paying down credit card balances may improve your credit score by lowering your credit utilization ratio and demonstrating responsible credit management.

A balance transfer may help reduce interest costs if you qualify for favorable terms. However, fees, promotional periods, and future interest rates should be considered carefully.