A USDA loan calculator helps estimate your monthly mortgage payment before you apply for a home loan backed by the U.S. Department of Agriculture. By entering the home price, interest rate, loan term, property taxes, homeowners insurance, and USDA guarantee fees, you can see a realistic estimate of your monthly housing costs. This makes it easier to compare homes, set a budget, and understand whether a property fits comfortably within your finances.

How a USDA Loan Calculator Works

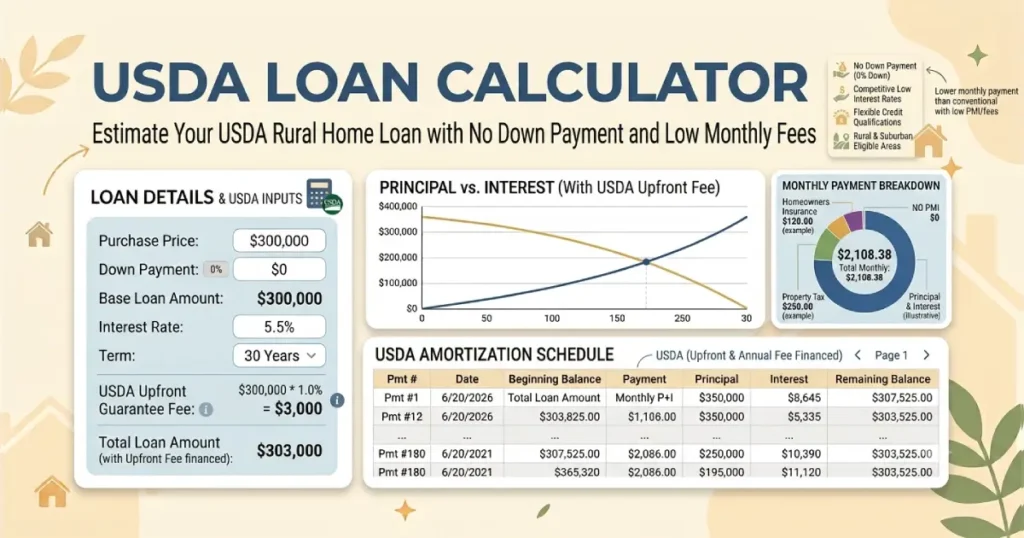

A USDA mortgage calculator combines several costs into one monthly payment estimate. Unlike a conventional mortgage, USDA loans include both an upfront guarantee fee and an annual guarantee fee that is paid monthly as part of your mortgage payment.

A complete estimate generally includes:

- Principal and interest

- Property taxes

- Homeowners insurance

- USDA mortgage calculator guarantee fees

- HOA dues, if applicable

The calculator provides an estimate rather than a final loan offer. Your lender will determine the exact payment after reviewing your credit, income, debt obligations, and the property you intend to purchase.

Information You'll Need

Providing accurate numbers produces a more useful estimate.

| Input | Why It Matters |

|---|---|

| Home price | Determines the loan amount. |

| Down payment | Many USDA loans require no down payment, but optional down payments reduce borrowing. |

| Interest rate | Has a significant impact on monthly payments. |

| Loan term | Typically 30 years for USDA home loans. |

| Property taxes | Varies by county and state. |

| Homeowners insurance | Required by lenders. |

| HOA fees | Included if the property belongs to a homeowners association. |

Understanding USDA Loan Costs

Principal and Interest

This is the portion of your payment that repays the amount borrowed plus interest charged by the lender.

Guarantee Fees

Instead of traditional mortgage insurance, USDA loans charge guarantee fees. The upfront fee is usually financed into the loan, while the annual fee is divided into monthly installments.

Escrow Costs

Most lenders collect property taxes and homeowners insurance through an escrow account, adding these expenses to your monthly payment.

Who Can Use a USDA Loan?

USDA loans are designed for eligible homebuyers purchasing homes in qualified rural and many suburban communities. Despite the name, many towns outside major metropolitan areas qualify.

General eligibility often includes:

- Buying a primary residence

- Meeting household income limits for the area

- Purchasing a property located within an eligible USDA area

- Demonstrating the ability to repay the loan

A mortgage calculator helps estimate affordability, but it cannot determine USDA eligibility by itself.

Benefits of Using a USDA Loan Payment Calculator

- Estimate monthly payments before speaking with a lender.

- Compare different purchase prices.

- Evaluate how changing interest rates affect affordability.

- See how property taxes influence total housing costs.

- Plan your monthly budget more accurately.

- Estimate the impact of adding a voluntary down payment.

Factors That Affect Your Monthly Payment

Interest Rate

Even a small difference in interest rates can significantly change your payment over a 30-year mortgage.

Home Price

A higher purchase price increases the loan balance and monthly payment.

Property Taxes

Taxes vary considerably by location. Two homes with identical prices can have noticeably different monthly costs.

Insurance Premiums

Insurance costs depend on the property's value, location, and coverage requirements.

HOA Fees

Neighborhood association dues should always be included when evaluating affordability.

How to Estimate an Affordable Home Price

Rather than starting with the maximum amount you qualify to borrow, begin with a monthly payment that comfortably fits your budget.

Many buyers use a calculator to test different scenarios by adjusting:

- Purchase price

- Interest rate

- Property taxes

- Insurance estimates

- Optional down payment

This approach often provides a clearer picture than focusing only on the loan amount.

Common Mistakes When Using a USDA Loan Calculator

- Using outdated property tax estimates.

- Leaving out homeowners insurance.

- Ignoring HOA dues.

- Assuming today's interest rate will still be available later.

- Forgetting to include USDA guarantee fees.

- Assuming eligibility without checking income and property requirements.

USDA Loan vs. Conventional Mortgage

| Feature | USDA Loan | Conventional Loan |

|---|---|---|

| Minimum down payment | Often 0% | Varies by lender and program |

| Property eligibility | Eligible rural and suburban areas | No location restrictions |

| Income limits | Yes | Generally no |

| Guarantee or mortgage insurance | USDA guarantee fees | May require private mortgage insurance depending on down payment |

Frequently Asked Questions

A calculator provides a reliable estimate when you enter realistic values for the purchase price, interest rate, taxes, insurance, and guarantee fees. Your lender's final loan estimate may differ because it reflects your credit profile, verified income, closing costs, and current market rates.

Yes. Including property taxes and homeowners insurance gives a more realistic estimate of your monthly housing payment. If the property has HOA dues, adding those costs provides an even clearer budgeting picture.

USDA loans do not use traditional private mortgage insurance. Instead, they include guarantee fees. Some calculators label this section as mortgage insurance for simplicity, but the fees are specific to the USDA loan program.

Yes. Many eligible borrowers finance 100% of the home's purchase price. Selecting a zero down payment provides an estimate that reflects one of the primary advantages of USDA financing.

Absolutely. Even a fraction of a percentage point can noticeably increase or reduce your monthly payment and the total interest paid over the life of the loan.

No. A calculator estimates payments but cannot determine eligibility. Income limits, property location, credit history, and debt obligations all influence whether you qualify for the program.

Yes. Running several scenarios helps identify a comfortable price range and shows how changes in home price affect monthly affordability without committing to a specific property.

If the home belongs to a homeowners association, including monthly dues provides a more complete estimate of your ongoing housing expenses and helps avoid budgeting surprises.

Most USDA loans allow additional principal payments without a prepayment penalty. Paying extra can reduce the loan balance faster and lower the total interest paid over time.

Lenders use verified financial information, current interest rates, actual property taxes, insurance quotes, and precise guarantee fee calculations. Online calculators are planning tools, while official loan estimates reflect the specific details of your application.