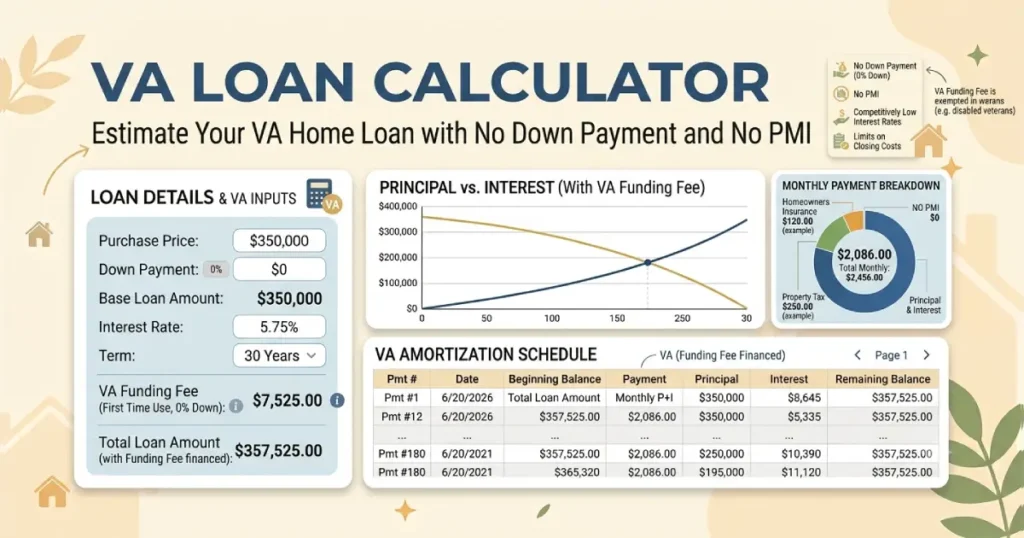

A VA loan calculator helps veterans, active-duty service members, and eligible military families estimate their monthly mortgage payments before applying for a VA home loan. By entering the home price, loan term, interest rate, property taxes, homeowners insurance, and VA funding fee, buyers can get a clearer picture of their expected housing costs and determine a realistic budget.

How a VA Loan Calculator Works

A VA mortgage payment estimate includes more than just principal and interest. A reliable calculation considers the main expenses that affect your monthly payment, including taxes, insurance, and the VA funding fee when applicable.

Most VA loan calculators consider:

- Home purchase price

- Down payment amount

- Interest rate

- Loan term

- Property taxes

- Homeowners insurance

- VA funding fee

The result is an estimate of your monthly housing cost. Your actual payment may vary based on lender terms, credit history, loan approval details, and the final property assessment.

What Information Do You Need for a VA Mortgage Calculator?

Accurate inputs create a more realistic estimate. Before using a calculator, gather the following information:

| Input | Purpose |

|---|---|

| Home price | Determines the amount you may need to borrow. |

| Down payment | Reduces the loan balance if you choose to make one. |

| Interest rate | Changes the monthly principal and interest payment. |

| Loan term | Most VA mortgages use a 15-year or 30-year term. |

| Taxes and insurance | Shows the complete monthly housing expense. |

| VA funding fee | Accounts for the one-time fee charged on many VA loans. |

Understanding VA Loan Monthly Payments

Principal and Interest

The largest portion of most mortgage payments goes toward repaying the borrowed amount and paying interest charged by the lender.

Property Taxes

Property taxes vary significantly depending on location. Including them in your estimate helps prevent underestimating your monthly costs.

Homeowners Insurance

Mortgage lenders generally require homeowners insurance to protect the property. Premiums depend on location, coverage level, and property characteristics.

VA Funding Fee

The VA funding fee helps support the VA loan program. Many borrowers finance this fee into their mortgage, although some veterans and service members may qualify for an exemption.

Benefits of Using a VA Loan Payment Calculator

A calculator can help you make better decisions before contacting lenders or shopping for homes.

- Estimate your expected monthly payment.

- Compare different home prices.

- Understand how interest rates affect affordability.

- See the impact of making a down payment.

- Plan your budget before starting the home search.

- Compare VA financing with other mortgage options.

VA Loan Eligibility Requirements

A VA loan calculator estimates payments, but it does not determine whether you qualify. Eligibility depends on factors such as military service history, discharge status, income, credit profile, and lender requirements.

Generally eligible borrowers may include:

- Veterans who meet service requirements

- Active-duty service members

- Certain National Guard and Reserve members

- Some surviving spouses

Borrowers must also purchase a primary residence that meets VA property requirements.

VA Loan vs Conventional Mortgage

| Feature | VA Loan | Conventional Loan |

|---|---|---|

| Down payment | Often no down payment required | Varies by lender and borrower profile |

| Mortgage insurance | No private mortgage insurance | May require PMI with a low down payment |

| Eligibility | Requires VA eligibility | Available to general borrowers |

| Property use | Primary residence | Primary homes and other property types depending on loan type |

Factors That Can Change Your VA Mortgage Payment

Interest Rate

Your interest rate has one of the biggest effects on the total cost of your mortgage. A lower rate can reduce monthly payments and long-term interest expenses.

Loan Amount

A higher purchase price creates a larger loan balance and increases the monthly payment.

Down Payment

Although many VA borrowers choose zero down financing, making a down payment can reduce the amount borrowed.

Credit Profile

Your credit history may influence the interest rate offered by lenders, which affects affordability.

Common Mistakes When Using a VA Mortgage Calculator

- Only calculating principal and interest while ignoring taxes and insurance.

- Using an unrealistic interest rate.

- Forgetting the VA funding fee.

- Assuming calculator results guarantee loan approval.

- Buying based only on the maximum loan amount instead of a comfortable payment.

Frequently Asked Questions

A VA loan calculator provides a useful estimate when you enter realistic information about the home price, interest rate, taxes, insurance, and funding fee. The final payment may differ because lenders use verified financial information and current loan terms.

Yes. Including property taxes and homeowners insurance creates a more accurate estimate of your total monthly housing expense. These costs can vary significantly depending on the location and property.

Many calculators include the VA funding fee because it can affect the total loan amount. However, some eligible borrowers may receive an exemption, which can change the final payment calculation.

Yes. Many eligible VA borrowers purchase homes with no down payment. A zero down payment calculation can help estimate the payment for a typical VA financing scenario.

The interest rate directly affects your monthly principal and interest payment. Even a small rate difference can change affordability and the total amount of interest paid throughout the loan.

No. A calculator only estimates payments. VA loan eligibility depends on military service requirements, income, credit history, and lender approval standards.

Yes. Estimating payments before shopping helps you understand your budget and avoid looking at homes that may create an uncomfortable monthly expense.

VA loans can provide valuable benefits, including no private mortgage insurance and flexible financing options. However, the best choice depends on your personal financial situation and available loan options.