A loan payoff calculator helps you estimate how quickly you can pay off a loan, how much interest you will pay over time, and how additional payments can shorten your repayment schedule. By entering your current loan balance, interest rate, monthly payment, and extra payments, you can create a clearer plan to reduce debt and understand the financial impact of paying your loan early.

How a Loan Payoff Calculator Works

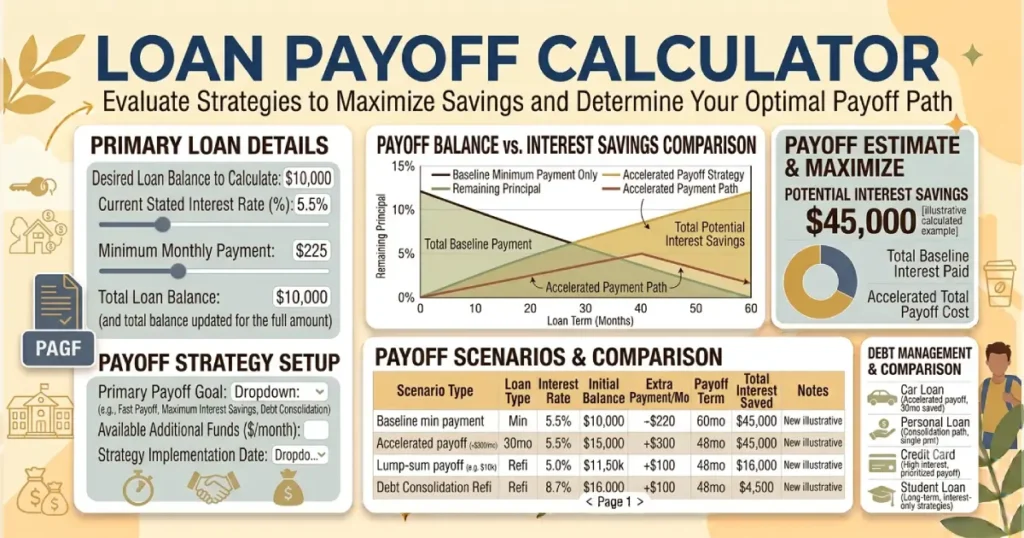

A loan payoff calculator estimates your remaining repayment timeline based on your outstanding balance, interest rate, and payment amount. It shows how long it may take to eliminate your loan and how much interest you may save by making additional payments.

The calculator can help you determine:

- How long to pay off a loan

- Loan payoff date

- Total remaining interest costs

- Impact of making extra payments

- Potential interest savings from early repayment

Loan payoff calculations are useful for mortgages, auto loans, personal loans, student loans, and other installment debts with scheduled payments.

The actual payoff amount may differ because lenders may calculate interest differently, charge fees, or apply payments according to specific loan agreements.

What Information Do You Need?

| Input | Description |

|---|---|

| Current loan balance | The remaining amount you still owe. |

| Interest rate | The annual percentage rate charged on the loan. |

| Current monthly payment | The amount you currently pay each month. |

| Extra payment amount | Additional money applied toward reducing the loan balance. |

| Loan type | Mortgage, auto loan, personal loan, student loan, or another installment loan. |

Why Use a Loan Payoff Calculator?

Many borrowers make regular payments without knowing exactly when their loan will be paid off or how much interest remains. A calculator provides a clearer picture of your repayment progress.

Common reasons to use a loan payoff calculator include:

- Finding your estimated debt-free date.

- Understanding remaining interest costs.

- Comparing different payment strategies.

- Seeing the effect of paying extra each month.

- Planning whether early repayment fits your financial goals.

- Reducing long-term borrowing costs.

How Extra Payments Affect Loan Payoff

Additional payments can reduce your principal balance faster, which may lower the amount of interest charged over the life of the loan.

For example, adding an extra amount to your monthly payment can shorten the repayment period because more money goes toward reducing the outstanding balance.

| Payment Strategy | Result |

|---|---|

| Regular payments only | Loan follows the original repayment schedule. |

| Small extra payments | May reduce repayment time and interest costs. |

| Larger additional payments | Can significantly accelerate payoff. |

Before making extra payments, check whether your lender charges any prepayment penalties or has specific rules for applying additional payments.

Loan Payoff vs Regular Loan Repayment

A standard loan repayment schedule is designed to pay off the balance over a fixed period. A payoff strategy focuses on reducing the loan faster by increasing payments or making additional contributions.

| Approach | Monthly Payment | Total Interest |

|---|---|---|

| Standard repayment | Usually lower | Higher over a longer period |

| Accelerated payoff | Higher | Usually lower |

The best approach depends on your cash flow, financial priorities, emergency savings, and other debts.

Types of Loans You Can Calculate

A loan payoff calculator can be used for many common types of debt:

- Mortgage payoff calculator – Estimates how additional payments may shorten your home loan.

- Auto loan payoff calculator – Shows how quickly you can eliminate vehicle financing.

- Personal loan payoff calculator – Helps estimate repayment progress on unsecured loans.

- Student loan payoff calculator – Helps borrowers estimate repayment timelines for education debt.

- Home equity loan payoff calculator – Calculates remaining repayment schedules for home-backed borrowing.

Factors That Affect Your Loan Payoff Time

Remaining Balance

The amount you still owe directly affects how long repayment will take. Larger balances generally require more time or higher payments to eliminate.

Interest Rate

A higher interest rate increases the cost of borrowing and can slow down payoff progress because more of each payment goes toward interest.

Monthly Payment Amount

Your monthly payment determines how quickly your principal balance decreases. Higher payments generally lead to faster payoff.

Additional Payments

Extra payments can reduce the principal balance faster and may lower total interest costs.

Loan Terms

The original loan length affects the repayment schedule and total interest paid throughout the loan.

Should You Pay Off Your Loan Early?

Paying off debt early can provide financial benefits, but it is not always the best choice for every borrower. Before making large additional payments, consider your overall financial situation.

Questions to consider:

- Do you have an emergency fund?

- Are you paying off higher-interest debt first?

- Are you saving enough for retirement?

- Does your loan have prepayment restrictions?

- Would investing the extra money provide a better opportunity?

A loan payoff calculator can help compare different scenarios before making a decision.

How to Pay Off a Loan Faster

- Make additional principal payments when possible.

- Increase your monthly payment amount.

- Apply unexpected income toward loan reduction.

- Refinance only when the new terms provide a clear benefit.

- Avoid extending the loan term unnecessarily.

- Track your progress regularly.

Even small additional payments can make a meaningful difference over the life of a loan.

Common Loan Payoff Mistakes

- Focusing only on the monthly payment instead of total interest.

- Ignoring the impact of additional payments.

- Paying off low-interest debt while carrying high-interest debt.

- Not checking lender rules for extra payments.

- Using all available cash to pay debt without keeping emergency savings.

Loan Payoff Calculator Example

Suppose you have a remaining loan balance of $25,000 with a fixed interest rate and monthly payments. A payoff calculator can show how adding an extra $100 per month may reduce your repayment timeline and lower the total interest paid.

| Loan Detail | Example |

|---|---|

| Remaining balance | $25,000 |

| Interest rate | 7% |

| Current payment | $500/month |

| Extra payment | $100/month |

The calculator helps visualize how small changes in payment habits can affect your overall debt timeline.

Frequently Asked Questions

A loan payoff calculator estimates how long it will take to repay a loan and how much interest you may pay based on your remaining balance, interest rate, and payment amount.

A loan payoff calculator uses your loan balance, interest rate, and monthly payments to estimate your remaining repayment schedule. It can also show how extra payments may speed up payoff.

You can pay off a loan faster by increasing monthly payments, making extra principal payments, reducing expenses, or applying additional income toward the loan balance.

Yes. Extra payments can reduce the principal balance faster, which may decrease the amount of interest charged over the remaining life of the loan.

Paying off a loan early may reduce interest costs and provide financial flexibility, but the decision depends on your savings, other debts, investment goals, and loan terms.

Yes. Many calculators allow you to enter additional payments to estimate how much faster you may repay your loan and how much interest you could save.

The payoff time depends on your remaining balance, interest rate, monthly payment, and any additional payments you make. A calculator can provide an estimate based on your inputs.

Refinancing may help if it lowers your interest rate or provides better repayment terms. However, extending the loan term may increase total interest costs.