Our House Affordability Calculator helps you estimate how much home you may be able to afford based on your income, monthly debts, down payment, loan term, and estimated mortgage interest rate. Whether you're buying your first home or planning your next move, understanding your budget before shopping can help you make confident financial decisions.

While many buyers begin by looking at home prices, lenders focus on your ability to comfortably repay the loan. This calculator estimates an affordable price range using common mortgage qualification factors, allowing you to compare different scenarios before applying for financing.

What Is a House Affordability Calculator?

A house affordability calculator estimates the maximum home price you may be able to purchase without exceeding recommended borrowing limits. Instead of looking only at the purchase price, it considers several financial factors that influence mortgage affordability.

Although every lender has its own underwriting standards, affordability estimates typically consider your income, recurring monthly debts, available down payment, estimated property taxes, homeowners insurance, and current mortgage interest rates.

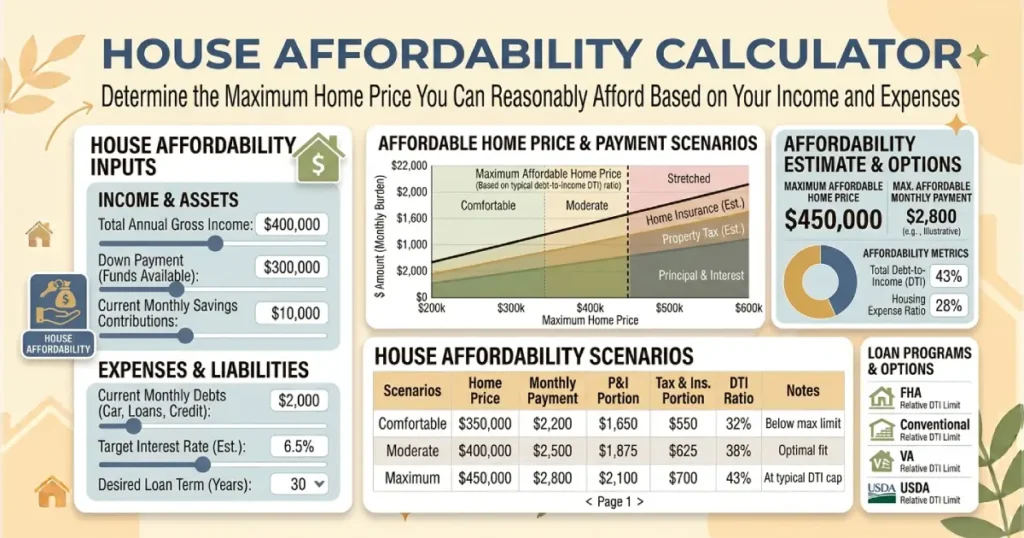

How the House Affordability Calculator Works

Our calculator combines your financial information with estimated mortgage costs to calculate an affordable home price.

Enter the following information:

- Annual household income

- Monthly debt payments

- Down payment amount

- Loan term

- Estimated interest rate

- Property taxes

- Homeowners insurance

- HOA dues (if applicable)

The calculator estimates your affordable purchase price, projected monthly mortgage payment, loan amount, and estimated debt-to-income ratio based on the information you provide.

What Determines Home Affordability?

Several financial factors influence how much home you can reasonably afford. Income is important, but lenders also evaluate your existing financial obligations and the overall risk of the loan.

The most significant factors include:

- Your annual household income.

- Your monthly debt obligations.

- Your available down payment.

- Your credit profile.

- Your mortgage interest rate.

- Estimated property taxes and insurance.

- The length of your mortgage.

Because these factors work together, increasing your down payment or reducing existing debt may significantly improve your purchasing power.

Understanding Debt-to-Income Ratio (DTI)

One of the most important measurements lenders use when evaluating mortgage applications is the debt-to-income ratio, commonly called DTI.

Your DTI compares your total monthly debt payments with your gross monthly income. A lower DTI generally indicates that you have more financial flexibility to manage a mortgage payment alongside your other financial responsibilities.

While acceptable DTI limits vary by lender and loan program, reducing debt before applying for a mortgage may improve both affordability and financing options.

Why Your Down Payment Matters

Your down payment directly affects how much you need to borrow. A larger down payment reduces your loan amount, lowers your monthly mortgage payment, and may decrease the total interest paid over the life of the loan.

Depending on your mortgage program, a larger down payment may also improve your loan terms or reduce the need for mortgage insurance.

Don't Forget the Other Costs of Homeownership

Many first-time buyers focus only on the monthly mortgage payment, but owning a home involves additional ongoing expenses.

- Property taxes.

- Homeowners insurance.

- Private mortgage insurance (when applicable).

- HOA fees.

- Utilities.

- Maintenance and repairs.

Including these expenses in your budget provides a more realistic picture of what you can comfortably afford.

Buying Within Your Budget

Qualifying for a larger mortgage doesn't always mean you should borrow the maximum amount available. Choosing a home that comfortably fits your budget may provide greater financial flexibility for future savings, emergencies, retirement planning, and other life goals.

Many financial experts recommend selecting a monthly housing payment that leaves room in your budget for unexpected expenses rather than stretching your finances to the lender's maximum approval amount.

How This Calculator Can Help

Using a house affordability calculator before speaking with a lender allows you to compare different purchase prices, down payment amounts, and mortgage terms without affecting your credit score.

You can quickly evaluate how changes in interest rates, income, or debt may influence your home-buying budget and determine a comfortable price range before beginning your home search.

Frequently Asked Questions

A house affordability calculator estimates how much home you may be able to afford based on your income, debts, down payment, estimated mortgage payment, and other housing expenses.

The answer depends on your income, monthly debt obligations, available down payment, mortgage interest rate, property taxes, homeowners insurance, and your lender's qualification requirements.

Yes. Your credit profile may influence the interest rate you qualify for, which affects your monthly payment and the total amount you can comfortably afford to borrow.

Your debt-to-income ratio helps lenders determine whether you can reasonably manage your mortgage payment alongside your existing financial obligations.

Not necessarily. Many buyers choose a lower purchase price to maintain greater financial flexibility and reduce long-term financial stress.

Yes. A larger down payment reduces your loan amount, lowers your monthly payment, and may improve your financing options depending on the loan program.

Yes. This calculator estimates affordability by considering housing expenses beyond the mortgage itself, including property taxes and homeowners insurance when applicable.

The calculator provides an estimate based on the information you enter. Your final mortgage approval, interest rate, and borrowing limit will depend on your lender's underwriting guidelines and your complete financial profile.