Our Refinance Calculator helps you estimate whether refinancing your mortgage could save you money. By comparing your current mortgage with a new loan, you can estimate your new monthly payment, potential interest savings, and the time it may take to recover your refinancing costs.

Whether you're looking for a lower interest rate, a shorter loan term, reduced monthly payments, or access to your home's equity through a cash-out refinance, using a mortgage refinance calculator is one of the easiest ways to compare different refinancing scenarios before speaking with a lender.

What Is Mortgage Refinancing?

Mortgage refinancing replaces your existing home loan with a new mortgage. Homeowners typically refinance to secure a lower interest rate, reduce their monthly payment, shorten the repayment term, switch between adjustable-rate and fixed-rate mortgages, or access equity through a cash-out refinance.

While refinancing can reduce borrowing costs, it also involves closing costs and lender fees. That's why using a refinance payment calculator before applying can help determine whether refinancing makes financial sense for your situation.

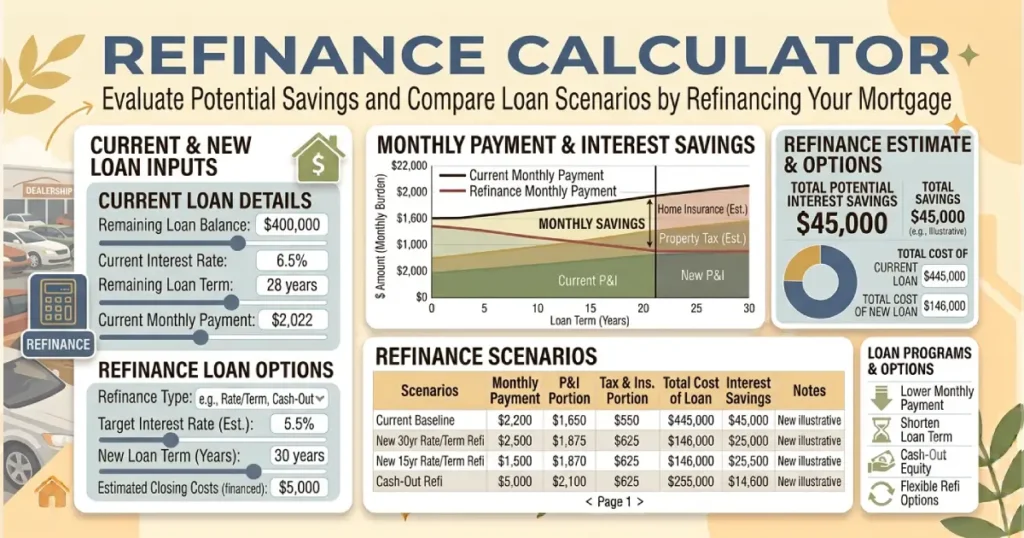

How Our Refinance Calculator Works

Our calculator compares your current mortgage with a potential new loan. By entering a few basic details, you can estimate the financial impact of refinancing.

Enter the following information:

- Current mortgage balance

- Current interest rate

- Remaining loan term

- New interest rate

- New loan term

- Estimated closing costs

- Cash-out amount (if applicable)

The calculator estimates your new monthly payment, lifetime interest costs, potential monthly savings, total interest savings, and your estimated break-even point.

When Does Refinancing Make Sense?

Refinancing may be beneficial when current mortgage rates are lower than your existing interest rate or when your financial goals have changed. Some homeowners refinance to lower monthly payments, while others choose a shorter loan term to pay off their mortgage sooner.

A refinance may also be worth considering if your credit score has improved since obtaining your original mortgage, allowing you to qualify for better loan terms.

Understanding the Break-Even Point

One of the most important factors when refinancing is calculating your break-even point. This represents the number of months required for your monthly savings to recover the upfront refinancing costs.

For example, if refinancing costs $4,000 and your new mortgage saves $200 per month, your break-even point would be approximately 20 months. If you expect to sell your home before reaching that point, refinancing may not provide meaningful financial benefits.

Common Reasons Homeowners Refinance

- Reduce monthly mortgage payments.

- Obtain a lower mortgage interest rate.

- Switch from an adjustable-rate mortgage (ARM) to a fixed-rate mortgage.

- Pay off the loan faster with a shorter mortgage term.

- Consolidate higher-interest debt through a cash-out refinance.

- Remove mortgage insurance after building sufficient home equity.

Rate-and-Term Refinance vs. Cash-Out Refinance

| Type | Purpose | Best For |

|---|---|---|

| Rate-and-Term Refinance | Replace your existing mortgage with improved loan terms. | Lower monthly payments or shorter repayment period. |

| Cash-Out Refinance | Borrow against your home's equity. | Home improvements, debt consolidation, or major expenses. |

Understanding the difference between these two options can help you choose the refinance strategy that best supports your financial goals.

Factors That Affect Your Refinance Savings

Several variables influence whether refinancing is worthwhile.

- Your current mortgage balance.

- Your current and new interest rates.

- The remaining loan term.

- Estimated closing costs.

- Your credit score.

- The amount of home equity you've built.

- Current market interest rates.

Even a relatively small reduction in your interest rate may result in significant savings over the life of your mortgage, especially for larger loan balances.

Should You Refinance Your Mortgage?

The answer depends on your financial goals. Some homeowners prioritize lower monthly payments, while others focus on reducing total interest costs or paying off their mortgage earlier.

Using a home refinance calculator allows you to compare multiple loan scenarios before committing to a refinance. By reviewing estimated payments, interest savings, and your break-even point, you can make a more informed borrowing decision.

Benefits of Using Our Mortgage Refinance Calculator

- Estimate your new monthly mortgage payment.

- Compare your current loan with a refinance offer.

- Calculate your break-even point.

- Estimate total interest savings.

- Compare different loan terms.

- Evaluate cash-out refinance scenarios.

Frequently Asked Questions

A refinance calculator estimates how replacing your current mortgage with a new loan may affect your monthly payment, total interest costs, and long-term savings.

Many homeowners consider refinancing when mortgage interest rates decline, their credit score improves, or they want to change their loan term or monthly payment.

Your savings depend on your current mortgage balance, interest rate, loan term, closing costs, and the terms of your new mortgage. A refinance calculator provides an estimate before you apply.

The break-even point is the number of months it takes for your monthly savings to offset the closing costs associated with refinancing.

A cash-out refinance replaces your existing mortgage with a larger loan, allowing you to receive the difference in cash by borrowing against your available home equity.

Applying for a refinance may result in a temporary credit inquiry, but the long-term impact depends on your overall credit profile and financial behavior.

Some lenders offer refinancing options for borrowers with lower credit scores, although interest rates and loan terms may be less favorable than those available to borrowers with stronger credit.

The calculator provides estimates based on the information you enter. Your actual loan terms, closing costs, interest rate, and monthly payment will depend on your lender and your financial qualifications.