Use our FHA Loan Calculator to estimate your monthly mortgage payment before applying for a Federal Housing Administration (FHA) loan. Whether you're purchasing your first home or comparing financing options, this calculator helps you estimate principal, interest, mortgage insurance, property taxes, homeowners insurance, and other housing costs.

An FHA loan can make homeownership more accessible by allowing lower down payments and more flexible credit requirements than many conventional mortgage programs. By using our FHA home loan calculator, you can better understand your estimated monthly payment and prepare for the financial responsibilities of buying a home.

What Is an FHA Loan?

An FHA loan is a government-insured mortgage backed by the Federal Housing Administration. Although the FHA does not lend money directly, it insures approved lenders against certain losses, making it easier for borrowers to qualify for financing.

Because the loan is insured by the government, FHA mortgages often allow lower down payments and more flexible qualification standards than conventional loans. This makes them especially popular among first-time home buyers and borrowers with limited savings or less-than-perfect credit histories.

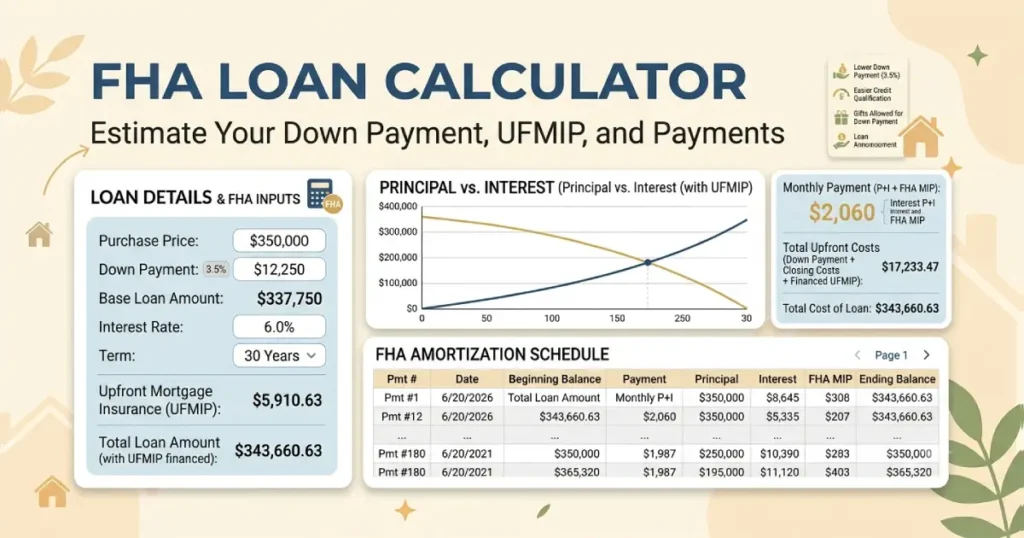

How the FHA Loan Calculator Estimates Your Payment

Our FHA loan payment calculator uses standard mortgage formulas to estimate your monthly payment based on the information you provide.

Simply enter:

- Home purchase price

- Down payment

- Loan term

- Interest rate

- Estimated annual property taxes

- Homeowners insurance

- Monthly HOA dues (if applicable)

- Mortgage insurance costs

After entering your information, the calculator estimates your monthly housing payment and provides a breakdown of the different costs included in your mortgage.

What Is Included in an FHA Mortgage Payment?

Your monthly mortgage payment usually consists of several different components rather than just repaying the loan itself.

- Principal – The portion that reduces your loan balance.

- Interest – The cost of borrowing money.

- Mortgage Insurance Premium (MIP) – Required for most FHA loans.

- Property Taxes – Local taxes based on your home's assessed value.

- Homeowners Insurance – Insurance protecting your home against covered losses.

- HOA Fees – Monthly homeowners association dues, if applicable.

Understanding these costs provides a more realistic estimate of your monthly housing expenses.

Mortgage Insurance on FHA Loans

One important feature of FHA loans is Mortgage Insurance Premium (MIP). Unlike many conventional mortgages that may require Private Mortgage Insurance (PMI), FHA loans generally require MIP regardless of the size of your down payment.

Mortgage insurance helps reduce risk for lenders and makes FHA financing available to more borrowers. Depending on your loan, you may pay both an upfront mortgage insurance premium and an annual premium that is divided into monthly payments.

Including mortgage insurance in your payment estimate helps you understand the true cost of an FHA mortgage before applying.

Who Should Consider an FHA Loan?

An FHA mortgage may be a suitable option for borrowers who meet one or more of the following situations:

- First-time home buyers.

- Borrowers with limited savings for a down payment.

- Home buyers with moderate credit scores.

- Individuals seeking more flexible qualification requirements.

- Buyers purchasing a primary residence.

Every borrower has a unique financial situation, so comparing FHA loans with conventional mortgage options is often a smart step before making a decision.

Factors That Affect Your FHA Loan Payment

Several factors influence the amount you'll pay each month.

- Purchase price of the home.

- Amount of your down payment.

- Mortgage interest rate.

- Length of the loan term.

- Mortgage insurance premiums.

- Property taxes.

- Homeowners insurance.

- HOA dues.

Even small changes in your interest rate or down payment can significantly affect your total monthly payment and the amount of interest paid over the life of the loan.

How Your Down Payment Changes Your Monthly Payment

Increasing your down payment generally reduces the amount you need to borrow, which lowers your monthly mortgage payment. A larger down payment may also reduce your long-term borrowing costs by decreasing the total interest paid over the life of the loan.

Using different down payment amounts in the calculator allows you to compare multiple home-buying scenarios before making a financial commitment.

Understanding Debt-to-Income Ratio

Mortgage lenders commonly review your debt-to-income ratio (DTI) when evaluating your loan application. Your DTI compares your monthly debt obligations to your gross monthly income.

A lower debt-to-income ratio generally indicates that you have more financial capacity to manage a mortgage payment. While qualifying requirements vary by lender, maintaining manageable debt levels may improve your borrowing options.

Using the Calculator Before Applying for a Mortgage

Estimating your payment before speaking with a lender helps you establish a realistic home-buying budget. You can compare different loan amounts, interest rates, and down payment options without affecting your credit score.

Many home buyers also use payment estimates when comparing FHA loans with VA loans, USDA loans, or conventional mortgage programs.

Frequently Asked Questions

An FHA loan calculator estimates your monthly mortgage payment using information such as the purchase price, down payment, loan term, interest rate, mortgage insurance, taxes, and homeowners insurance.

The amount you may qualify for depends on several factors, including your income, existing monthly debts, credit history, employment, available down payment, and lender guidelines. A calculator can estimate payments, but only a lender can determine your final loan approval.

Although many borrowers refer to it as PMI, FHA loans generally require Mortgage Insurance Premium (MIP). Your lender calculates the applicable mortgage insurance based on current FHA guidelines, your loan amount, and other qualifying factors. The annual premium is typically divided into monthly payments.

Most borrowers searching for PMI on FHA loans are actually referring to Mortgage Insurance Premium (MIP). The exact amount depends on FHA rules and your loan details, making an FHA loan calculator useful for estimating your monthly payment.

Divide your total monthly debt payments by your gross monthly income and multiply the result by 100. For example, if your monthly debts total $2,000 and your gross monthly income is $5,000, your debt-to-income ratio is 40%.

Many borrowers choose FHA financing because it generally allows lower down payments than conventional mortgage programs. Your eligibility depends on your financial profile and current lending requirements.

Most lenders collect property taxes and homeowners insurance through an escrow account, allowing these costs to be included in your monthly mortgage payment.

No. While FHA loans are popular with first-time buyers, eligible repeat home buyers may also qualify if they meet lender and FHA requirements.

Yes. Many homeowners refinance their FHA loan in the future to reduce their interest rate, shorten their loan term, or move into a conventional mortgage if it better fits their financial goals.

The calculator provides an estimate based on the information you enter. Your actual monthly payment may vary depending on your lender, current FHA mortgage insurance requirements, taxes, insurance costs, closing costs, and other applicable fees.