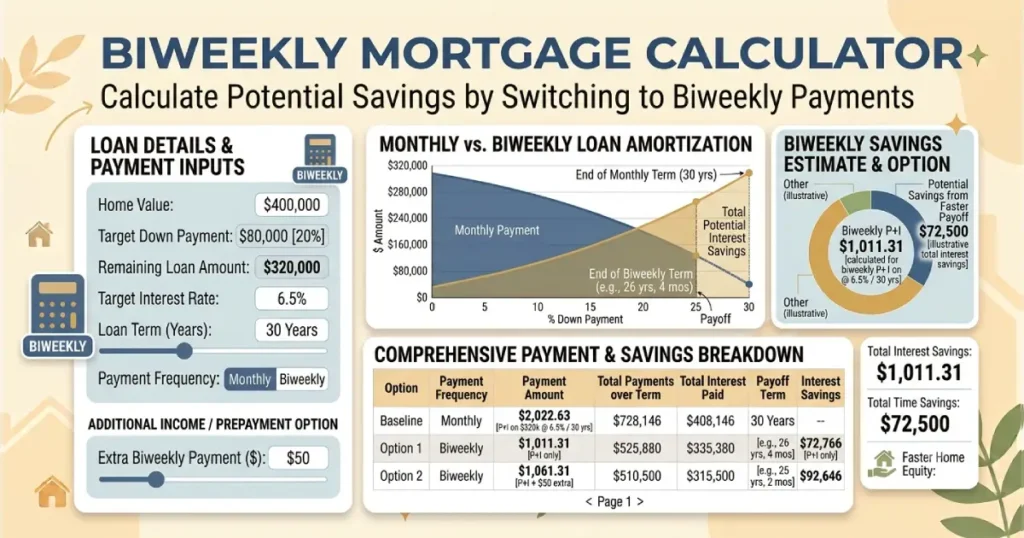

Our Biweekly Mortgage Calculator helps you estimate how switching from monthly mortgage payments to biweekly payments could affect your loan. By comparing both repayment schedules, you can estimate your potential interest savings, see how much sooner you might pay off your mortgage, and better understand the long-term impact of making more frequent payments.

For many homeowners, paying every two weeks is a simple strategy that fits naturally with a biweekly paycheck. While it doesn't reduce your interest rate, it may reduce the total interest paid because you gradually pay down your loan balance faster than with a standard monthly payment schedule. Whether you're buying a new home or looking for ways to become mortgage-free sooner, a biweekly mortgage payment calculator can help you compare your options before making changes to your repayment plan.

What Is a Biweekly Mortgage Payment?

A biweekly mortgage payment means paying half of your regular monthly mortgage payment every two weeks instead of making one full payment each month. Since there are 52 weeks in a year, you'll make 26 half-payments annually, which equals 13 full monthly payments instead of 12. That extra payment is one of the main reasons many homeowners choose a biweekly repayment strategy.

The additional annual payment reduces your principal balance sooner. Because mortgage interest is calculated on the remaining loan balance, reducing your principal earlier may lower the total interest paid over the life of the loan.

How the Biweekly Mortgage Calculator Works

This calculator estimates your mortgage using the same basic loan information used for a traditional mortgage calculation. Enter your loan amount, interest rate, repayment term, and payment frequency to compare monthly and biweekly repayment schedules.

The calculator estimates:

- Your standard monthly mortgage payment.

- Your biweekly payment amount.

- Total interest paid under each repayment method.

- Your estimated mortgage payoff date.

- Potential interest savings.

- Potential reduction in loan term.

These estimates provide a helpful comparison, although your actual savings depend on your lender's payment processing policies and the terms of your mortgage agreement.

Why Can Biweekly Payments Save Money?

The biggest advantage of biweekly payments isn't that interest is calculated differently—it's that you effectively make one extra mortgage payment each year. That additional payment goes toward reducing your loan balance faster, which decreases the amount of interest charged over time.

For example, imagine your monthly mortgage payment is $2,400. Instead of paying that amount once each month, you would pay $1,200 every two weeks. Over the course of one year, you'll make 26 half-payments, totaling $31,200 instead of $28,800. The difference equals one extra monthly payment applied toward your mortgage principal.

Monthly vs. Biweekly Mortgage Payments

| Feature | Monthly | Biweekly |

|---|---|---|

| Payments Per Year | 12 | 26 Half-Payments (13 Full Payments) |

| Principal Reduction | Standard | Accelerated |

| Interest Paid | Higher Over Time | Potentially Lower |

| Loan Payoff | Original Schedule | May Be Earlier |

Will Every Lender Process Biweekly Payments the Same Way?

Not necessarily. Before switching to biweekly payments, check with your mortgage servicer to understand how your payments are applied.

Some lenders immediately apply each payment toward your principal as it is received. Others may hold partial payments until the full monthly payment amount has been collected. In that situation, the financial benefit of paying every two weeks may be smaller than expected. The Consumer Financial Protection Bureau also recommends checking whether your lender charges fees for participating in a biweekly payment program.

Can You Achieve the Same Result Without a Biweekly Plan?

In many cases, yes. Some homeowners simply make one additional principal payment each year or divide that extra payment across twelve monthly payments. Depending on how your lender applies additional principal payments, the overall financial result may be similar to following an official biweekly payment schedule.

The best approach depends on your mortgage terms, budgeting preferences, and whether your lender offers a biweekly payment program without additional fees.

Who Should Consider Biweekly Mortgage Payments?

- Homeowners who want to pay off their mortgage earlier.

- Borrowers looking to reduce total interest costs.

- People paid every two weeks who prefer matching mortgage payments with their paycheck schedule.

- Homeowners planning to build equity faster.

- Borrowers who want a disciplined approach to making extra principal payments.

Frequently Asked Questions

A biweekly mortgage calculator estimates how making half of your monthly mortgage payment every two weeks could affect your payoff date and total interest costs compared with making one payment each month.

Instead of making 12 monthly payments each year, you make 26 half-payments. This equals 13 full monthly payments annually, allowing you to reduce your mortgage balance more quickly.

In many cases, yes. Because you effectively make one extra monthly payment each year, your loan balance decreases faster, which may shorten your repayment period.

They can. Paying down your principal sooner may reduce the amount of interest that accrues over the life of the mortgage. The exact savings depend on your loan amount, interest rate, and how your lender processes payments.

Many lenders allow borrowers to change their payment schedule or make additional principal payments, but policies vary. Contact your mortgage servicer before changing your repayment plan.

Some lenders charge enrollment or servicing fees for biweekly payment programs, while others may hold partial payments until your monthly due date. Review your mortgage agreement before enrolling.

For many borrowers, the financial outcome is very similar because both approaches result in paying additional principal. The better choice depends on your lender's policies and your personal budgeting preferences.

The calculator provides an estimate based on the information you enter. Your actual savings may differ depending on your loan agreement, payment timing, fees, escrow requirements, and how your lender applies additional payments.