A debt payoff calculator helps you estimate how long it may take to eliminate your debt, how much interest you could pay, and how different repayment strategies can affect your financial goals. By entering your balances, interest rates, and monthly payments, you can create a clearer plan to become debt-free.

How a Debt Payoff Calculator Works

A debt payoff calculator analyzes your current debt situation and estimates your repayment timeline based on your balances, interest rates, and payment amounts.

It can help you understand:

- How long it will take to pay off debt

- Debt payoff timeline

- Total interest you may pay

- How increasing payments affects your payoff date

- The difference between different debt repayment methods

The calculator works by applying your monthly payments toward your outstanding balances while accounting for the interest that accumulates over time.

Actual results may vary depending on lender policies, changing interest rates, fees, and whether you continue adding new debt.

What Information Do You Need?

| Input | Description |

|---|---|

| Debt balance | The amount you currently owe on each account. |

| Interest rate | The annual percentage rate charged on the debt. |

| Minimum payment | The required payment amount for each debt. |

| Extra payment | Additional money you can put toward debt repayment. |

| Debt type | Credit cards, personal loans, student loans, auto loans, or other balances. |

Why Use a Debt Payoff Calculator?

Many people know how much debt they owe but do not know how long repayment will take or how much interest they may pay. A calculator turns your current balances into a practical repayment forecast.

Common reasons to use a debt payoff calculator include:

- Creating a realistic debt repayment plan.

- Estimating your debt-free date.

- Comparing repayment strategies.

- Understanding the cost of interest.

- Seeing the impact of extra payments.

- Prioritizing which debts to pay first.

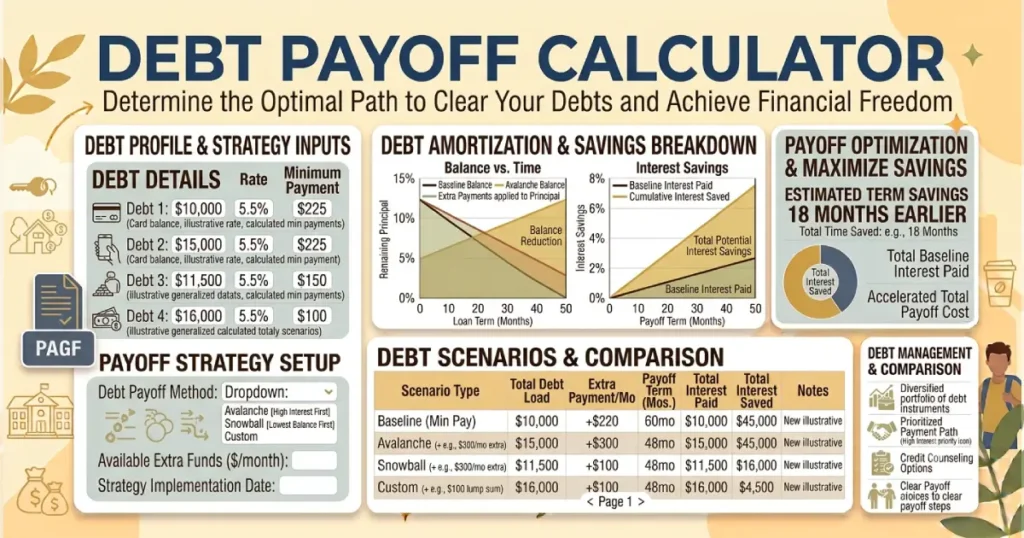

Debt Snowball vs Debt Avalanche Method

Two popular approaches for paying off debt are the debt snowball method and the debt avalanche method. Both can help organize repayment, but they prioritize debts differently.

| Method | How It Works | Main Benefit |

|---|---|---|

| Debt Snowball | Pays the smallest balance first while making minimum payments on other debts. | Creates quick progress and motivation. |

| Debt Avalanche | Pays the highest interest debt first while maintaining other payments. | Usually saves more money on interest. |

The best method depends on your financial priorities. Some people prefer the mathematical savings of the avalanche method, while others prefer the psychological benefits of quick wins.

How Debt Payoff Calculations Work

Debt repayment calculations consider your balance, interest rate, and payment amount. When you make a payment, part of the money covers interest charges and the remaining amount reduces your principal balance.

For example, a debt with a high interest rate can take much longer to eliminate if you only make minimum payments. Increasing your monthly payment can reduce both the repayment period and total interest cost.

| Payment Strategy | Impact |

|---|---|

| Minimum payments only | Longer repayment period and higher interest costs. |

| Fixed extra payments | Faster payoff and reduced interest. |

| Lump-sum payments | Immediate reduction of principal balance. |

Types of Debt You Can Include

A debt payoff calculator can be used for many types of consumer debt, including:

- Credit card debt

- Personal loans

- Student loans

- Auto loans

- Medical debt

- Store credit accounts

Tracking multiple debts together can help you see your complete financial picture and create a coordinated repayment strategy.

Factors That Affect Your Debt Payoff Timeline

Total Debt Balance

The amount you owe directly affects how long repayment takes. Larger balances generally require more time or larger payments to eliminate.

Interest Rates

High-interest debt grows faster because more of your payment goes toward interest instead of reducing the balance.

Monthly Payment Amount

Your payment amount is one of the biggest factors affecting your payoff timeline. Even small increases can reduce repayment time.

New Borrowing

Adding new debt while paying off existing balances can slow progress and increase total costs.

Consistency

Regular payments are essential for reducing debt. Missed payments can increase costs through fees and additional interest.

How to Pay Off Debt Faster

- Create a detailed budget and identify extra money for payments.

- Pay more than the minimum whenever possible.

- Focus additional payments on high-interest debt.

- Avoid adding new balances while repaying existing debt.

- Automate payments to stay consistent.

- Review your progress regularly.

A debt payoff calculator with extra payments can show how increasing your monthly contribution may shorten your repayment timeline.

Debt Consolidation and Payoff Planning

Debt consolidation combines multiple debts into a single payment, often through a personal loan or another financial product. Depending on the interest rate, fees, and repayment terms, consolidation may simplify payments or reduce borrowing costs.

Before consolidating debt, consider:

- The new interest rate.

- Loan fees.

- Repayment timeline.

- Whether monthly payments fit your budget.

- The risk of accumulating new debt.

Common Debt Payoff Mistakes

- Only making minimum payments without a repayment strategy.

- Ignoring interest rates.

- Paying random debts without prioritization.

- Taking on new debt while repaying old balances.

- Not tracking progress.

- Choosing a repayment plan that does not fit your budget.

Debt Payoff Calculator Example

Suppose you have multiple debts with different balances and interest rates. A calculator can help compare whether paying the highest-interest account first or the smallest balance first may lead to faster progress.

| Debt | Balance | Interest Rate |

|---|---|---|

| Credit card | $5,000 | 22% |

| Personal loan | $8,000 | 10% |

| Auto loan | $15,000 | 6% |

Seeing all debts together can make it easier to decide where additional payments should go.

Frequently Asked Questions

A debt payoff calculator estimates how long it will take to eliminate your debt and how much interest you may pay based on your balances, interest rates, and monthly payments.

A debt payoff calculator uses your debt balances, interest rates, and payment amounts to estimate your repayment timeline. It shows how different payment strategies may affect your debt-free date.

The time required depends on your total balance, interest rates, and monthly payments. Paying more than the minimum can significantly reduce the time needed to become debt-free.

The fastest approach usually involves increasing payments, avoiding new debt, and prioritizing high-interest balances. The debt avalanche method is often effective for reducing interest costs.

The debt avalanche method focuses on saving money by paying high-interest debt first. The debt snowball method focuses on paying smaller balances first to create motivation and momentum.

Yes. Extra payments reduce your principal balance faster, which can lower the amount of interest charged and shorten the repayment period.

Many debt payoff calculators allow multiple balances, interest rates, and payment amounts. This helps create a complete repayment plan across different accounts.

Debt consolidation may help simplify payments or reduce interest costs for some borrowers. However, the benefits depend on the new loan terms, fees, and repayment habits.

You can speed up repayment by increasing payments, reducing expenses, prioritizing expensive debt, and maintaining consistent payment habits.