A personal loan calculator helps estimate your monthly payments, total interest costs, and overall repayment amount before you borrow money. By entering your loan amount, interest rate, and repayment term, you can understand how much a personal loan may cost and compare different borrowing options before making a financial decision.

How a Personal Loan Calculator Works

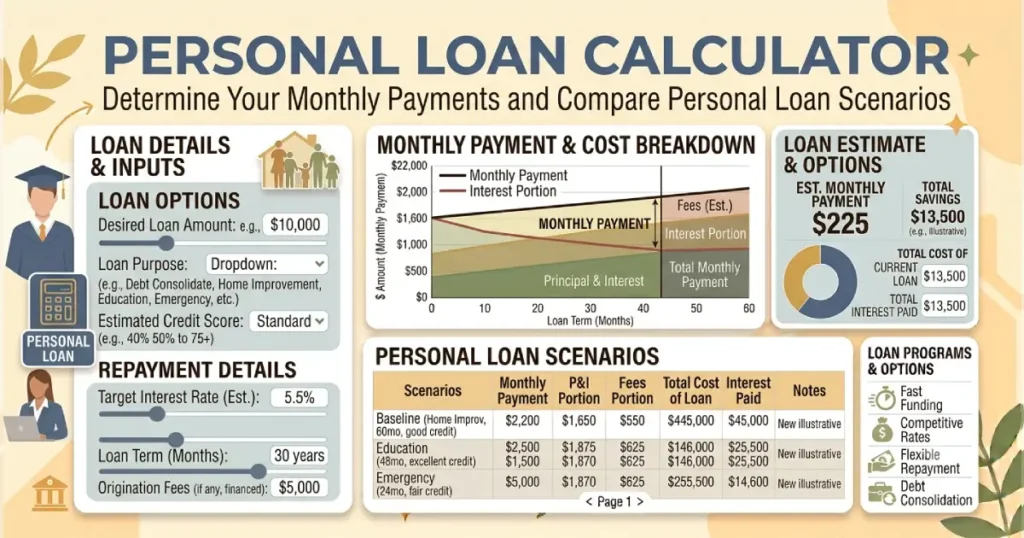

A personal loan calculator estimates your repayment schedule using three main factors: the amount borrowed, the loan interest rate, and the repayment period. Most personal loans are installment loans with fixed monthly payments over a specific term. :contentReference[oaicite:0]{index=0}

The calculator typically estimates:

- Personal loan monthly payment

- Total interest paid

- Total repayment cost

- Loan payoff date

- Impact of different loan terms

The basic calculation uses the loan principal, annual percentage rate (APR), and repayment length to determine the monthly payment amount.

Your actual payment may vary depending on lender fees, credit score, income, loan terms, and other factors considered during approval. :contentReference[oaicite:1]{index=1}

What Information Do You Need?

| Input | Description |

|---|---|

| Loan amount | The amount of money you plan to borrow. |

| Interest rate or APR | The cost of borrowing expressed as a percentage. |

| Loan term | The amount of time you have to repay the loan. |

| Origination fee | An upfront lender fee that may increase the total borrowing cost. |

| Extra payments | Additional payments that may reduce interest and shorten repayment time. |

Loan amount, APR, and repayment term are the biggest factors affecting your monthly payment and total loan cost. :contentReference[oaicite:2]{index=2}

How Personal Loan Payments Are Calculated

Most personal loans use fixed monthly payments, meaning your payment amount usually stays the same throughout the repayment period. Each payment includes a portion that goes toward interest and a portion that reduces your loan balance.

For example, a $15,000 loan with a five-year repayment term will generally have lower monthly payments than the same loan repaid over three years. However, the longer loan term usually results in paying more interest overall.

| Loan Term | Monthly Payment | Total Interest Cost |

|---|---|---|

| Shorter term | Higher monthly payment | Usually lower total interest |

| Longer term | Lower monthly payment | Usually higher total interest |

Understanding APR vs Interest Rate

When comparing personal loans, it is important to look beyond the advertised interest rate. The personal loan APRreflects the borrowing cost more completely because it may include certain fees associated with the loan.

A lower interest rate does not always mean a cheaper loan if the lender charges significant upfront fees. Comparing APRs can help you evaluate the true cost of different loan offers. :contentReference[oaicite:3]{index=3}

Common Uses for Personal Loans

Personal loans are often used for expenses that require a larger amount of money than someone may have available immediately. Common reasons borrowers use personal loans include:

- Debt consolidation

- Home improvement projects

- Medical expenses

- Major purchases

- Unexpected emergency costs

- Large personal expenses

Because personal loans usually have fixed repayment schedules, borrowers can know their expected monthly payment before accepting the loan.

Factors That Affect Personal Loan Rates

Credit Score

Your credit history and credit score can influence the interest rate and loan terms you receive. Borrowers with stronger credit profiles often qualify for more competitive rates.

Income and Debt

Lenders typically review your income and existing debts to evaluate whether you can comfortably manage additional monthly payments.

Loan Amount

A larger loan amount may increase your monthly payment and total interest cost, especially if combined with a longer repayment period.

Loan Term

A longer repayment term lowers the monthly payment but may increase the total amount of interest paid over the life of the loan.

Fees

Origination fees and other charges can increase the overall cost of borrowing. Some lenders include fees while others may not charge them.

Personal Loan Example Calculation

Consider a borrower taking out a $10,000 personal loan with a fixed interest rate and a five-year repayment term.

| Loan Detail | Example |

|---|---|

| Loan amount | $10,000 |

| Repayment term | 60 months |

| Interest rate | 10% |

| Payment type | Fixed monthly payments |

The calculator helps estimate the monthly payment and shows how much of the total repayment comes from borrowed money versus interest charges.

Why Use a Personal Loan Calculator?

- Estimate your expected monthly payment.

- Compare different repayment terms.

- Understand total borrowing costs.

- Determine whether a loan fits your budget.

- Compare loan offers from different lenders.

- Plan debt consolidation strategies.

Using a calculator before applying can help you avoid borrowing more than you can comfortably repay.

How to Reduce the Cost of a Personal Loan

- Improve your credit score before applying.

- Compare multiple lenders and loan offers.

- Choose the shortest affordable repayment term.

- Avoid borrowing more than necessary.

- Make extra payments when possible.

- Review fees before accepting a loan.

Even small differences in interest rates or repayment terms can significantly change the total cost of borrowing.

Common Personal Loan Mistakes

- Focusing only on the monthly payment instead of total cost.

- Ignoring APR and additional fees.

- Choosing a longer loan term without considering interest costs.

- Borrowing more than needed.

- Missing payments, which can damage credit history.

Frequently Asked Questions

A personal loan calculator estimates your monthly payment and total repayment cost using your loan amount, interest rate, and repayment term. It helps borrowers understand the financial impact before applying for a loan.

Your personal loan monthly payment depends on the amount borrowed, APR, and repayment length. A calculator uses these details to estimate the fixed payment required to repay the loan over time.

A good personal loan APR depends on your credit profile, income, lender, and market conditions. Borrowers with stronger credit generally qualify for lower rates, while higher-risk borrowers may receive higher APR offers.

Some personal loan calculators include origination fees and other costs, while basic calculators may only estimate principal and interest. Including fees provides a more accurate estimate of the total borrowing cost.

The amount you can afford depends on your income, monthly expenses, existing debts, and financial goals. A calculator can help estimate payments, but your overall budget should determine the appropriate loan amount.

No. Using a calculator does not affect your credit score because it does not involve a credit application or credit inquiry. Applying for a loan may involve a credit check depending on the lender.

A longer repayment term usually lowers your monthly payment but increases the total interest you pay. A shorter term can reduce borrowing costs but requires a higher monthly payment.

Many personal loans allow early repayment, but you should check your loan agreement for possible prepayment penalties or fees. Paying extra toward principal may reduce interest costs if allowed.