Our Extra Payment Mortgage Calculator helps you estimate how making additional mortgage payments could reduce your loan balance, shorten your repayment period, and lower the total interest paid over the life of your mortgage. Whether you're planning to contribute an extra amount every month, make annual lump-sum payments, or occasionally pay more toward your principal, this calculator provides a clear picture of the potential long-term savings.

Many homeowners focus on finding a lower interest rate, but making consistent extra principal payments can also be an effective strategy for reducing borrowing costs. Even relatively small additional payments may significantly decrease the amount of interest paid while helping you become mortgage-free sooner.

What Is an Extra Mortgage Payment?

An extra mortgage payment is any amount you pay in addition to your required monthly mortgage payment. Unlike your scheduled payment, which covers principal, interest, and often taxes and insurance, an extra payment is typically applied directly toward your loan principal.

Reducing your principal balance earlier means future interest is calculated on a smaller loan balance. Over time, this can lead to substantial interest savings and a shorter repayment period. Mortgage amortization schedules naturally shift more of each payment toward principal as the loan matures, and making extra payments accelerates that process.

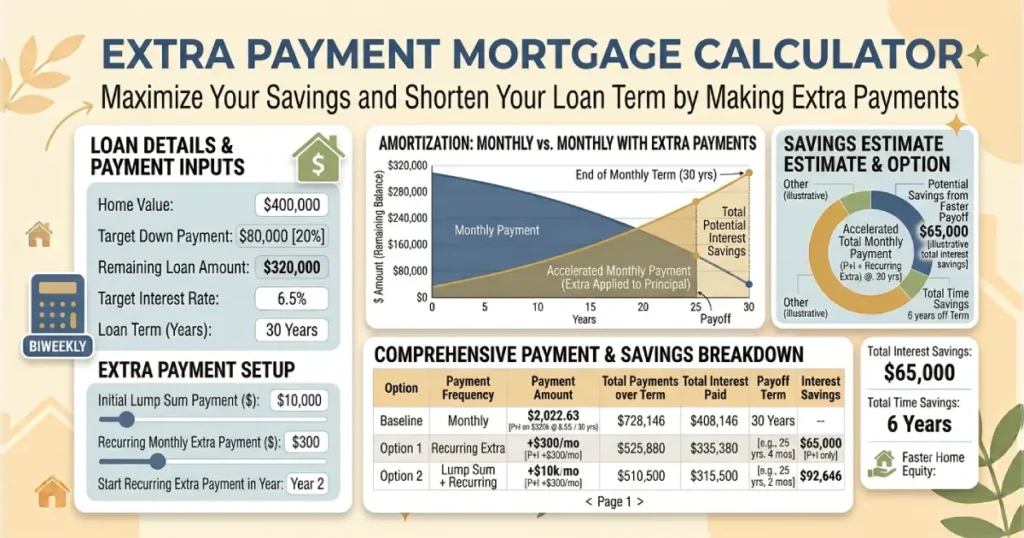

How the Extra Payment Mortgage Calculator Works

Our calculator compares your original mortgage repayment schedule with a revised schedule that includes additional payments. After entering your loan details, you'll instantly see how extra payments affect your mortgage over time.

Enter the following information:

- Original loan amount

- Interest rate

- Loan term

- Current loan balance (optional)

- Extra payment amount

- Payment frequency (monthly, yearly, or one-time)

The calculator estimates your updated payoff date, total interest paid, estimated interest savings, and the number of years you may save by making additional payments.

Why Extra Payments Can Save You Money

Mortgage interest is calculated using your remaining loan balance. As your principal decreases, the amount of interest charged also declines. Making additional payments reduces your balance faster, allowing more of each future payment to go toward principal instead of interest.

For borrowers with higher interest rates or longer loan terms, even modest extra payments may produce meaningful savings over several decades.

Monthly vs. Annual vs. One-Time Extra Payments

| Payment Strategy | How It Works | Potential Benefit |

|---|---|---|

| Monthly Extra Payment | Add a fixed amount every month. | Consistent principal reduction. |

| Annual Extra Payment | Make one additional payment each year. | Good for annual bonuses or tax refunds. |

| One-Time Lump Sum | Apply a large payment once. | Immediate reduction of loan balance. |

Each strategy can reduce interest costs. The best choice depends on your cash flow and long-term financial goals.

Should You Make Extra Mortgage Payments?

Paying extra toward your mortgage isn't always the right choice for every homeowner. Before committing additional funds, consider your emergency savings, high-interest debt, retirement contributions, and other financial priorities.

If your mortgage carries a relatively high interest rate, paying extra toward principal may provide a guaranteed return by reducing future interest expenses. On the other hand, homeowners with very low mortgage rates may decide that investing excess cash elsewhere better aligns with their financial objectives.

Check Your Lender's Payment Policy

Before making additional mortgage payments, confirm how your lender applies them. Ideally, extra funds should be credited directly toward your principal balance.

Some mortgage servicers require borrowers to specify that an additional payment is intended for principal reduction. If no instructions are provided, the payment may instead be applied toward future scheduled payments, reducing the financial benefit of paying extra.

Are There Prepayment Penalties?

Most modern residential mortgages allow borrowers to make additional principal payments without penalties. However, some loans may include prepayment penalty provisions, particularly during the first few years of the mortgage.

Review your mortgage documents or contact your lender before making large lump-sum payments to determine whether any restrictions apply.

Benefits of Using an Extra Payment Mortgage Calculator

- Estimate how much interest you could save.

- See how quickly additional payments reduce your loan balance.

- Compare different payment strategies before making financial decisions.

- Estimate your revised mortgage payoff date.

- Understand the long-term impact of paying extra toward principal.

Who Should Use This Calculator?

- Homeowners planning to pay off their mortgage early.

- Borrowers receiving annual bonuses or tax refunds.

- People considering lump-sum principal payments.

- Homeowners comparing refinancing with accelerated repayment.

- Anyone interested in reducing total mortgage interest.

Frequently Asked Questions

An extra payment mortgage calculator estimates how additional payments toward your mortgage principal can affect your loan payoff date and total interest costs.

In most cases, yes. However, you should verify with your lender that any additional payment is applied directly to your principal balance rather than toward future scheduled payments.

The amount depends on your loan balance, interest rate, repayment term, and how much extra you pay. Even relatively small monthly principal payments can save thousands of dollars in interest over time.

Monthly extra payments begin reducing your principal sooner, while annual lump-sum payments can also provide meaningful savings. The best option depends on your income and budgeting preferences.

The answer depends on your mortgage interest rate, investment goals, risk tolerance, and overall financial situation. Some homeowners prioritize becoming debt-free, while others may earn a higher long-term return through investing.

The calculator provides estimates based on the information you enter. Your actual savings may vary depending on your lender's payment processing policies, loan terms, escrow requirements, and any applicable fees.