Our Down Payment Calculator helps you estimate how much money you’ll need upfront when purchasing a home. Whether you’re buying your first house, upgrading to a larger property, or comparing different mortgage options, understanding your down payment is one of the most important steps in the home-buying process.

A larger down payment can reduce your monthly mortgage payment, lower your borrowing costs, and improve your chances of qualifying for favorable loan terms. Use this calculator to compare different down payment amounts and see how they affect your estimated loan amount before applying for a mortgage.

What Is a Down Payment?

A down payment is the portion of a home’s purchase price that you pay out of pocket at closing. The remaining balance is typically financed through a mortgage loan.

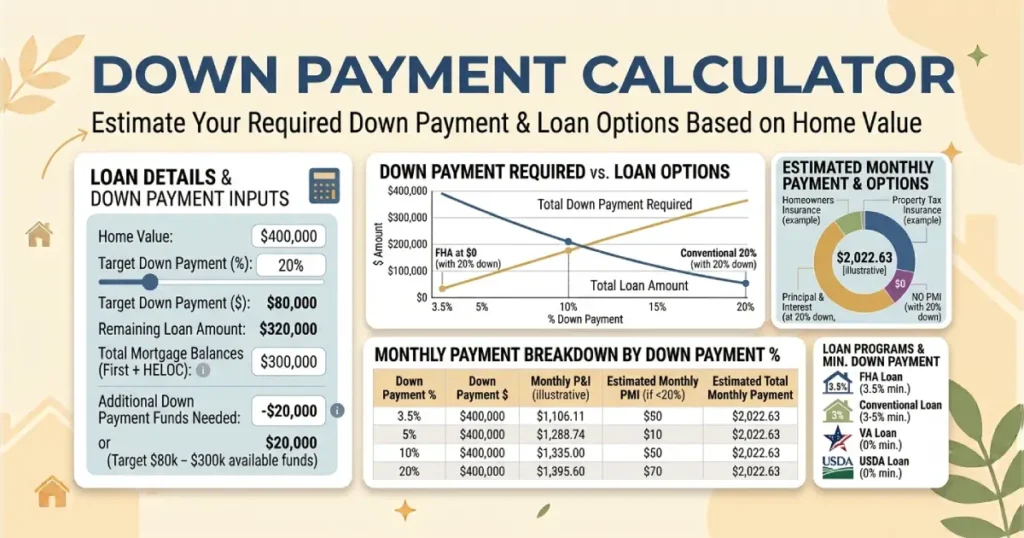

For example, if you’re buying a $400,000 home and make a 20% down payment, you’ll pay $80,000 upfront and borrow the remaining $320,000 through your mortgage lender.

Your down payment plays an important role in determining your loan amount, monthly mortgage payment, interest costs, and whether mortgage insurance may be required.

How the Down Payment Calculator Works

Our calculator estimates your required down payment using the home’s purchase price and the percentage or dollar amount you plan to contribute.

Simply enter:

- Home purchase price

- Down payment percentage or dollar amount

- Estimated interest rate

- Loan term

The calculator instantly estimates your down payment, remaining loan balance, and provides an overview of how different down payment amounts can affect your mortgage.

How Much of a Down Payment Do I Need for a House?

One of the most common questions home buyers ask is, “How much of a down payment do I need for a house?” The answer depends on several factors, including the type of mortgage, your lender’s requirements, and your financial situation.

While many buyers associate home purchases with a 20% down payment, that isn’t always required. Some loan programs allow qualified borrowers to purchase a home with a significantly smaller down payment. However, putting more money down generally reduces your loan balance and may lower your monthly payment and total interest costs.

Minimum Down Payment for a House

The minimum down payment for a house depends on the mortgage program you choose. Conventional, FHA, VA, and USDA loans each have different eligibility requirements and minimum down payment guidelines.

Even if you qualify for a low down payment program, contributing more upfront may help reduce your monthly payment, improve your loan-to-value ratio (LTV), and potentially lower borrowing costs over the life of your mortgage.

Benefits of Making a Larger Down Payment

- Borrow less money.

- Lower your monthly mortgage payment.

- Reduce the total interest paid over the life of the loan.

- Build home equity immediately.

- Improve your chances of receiving favorable loan terms.

- Potentially reduce or eliminate mortgage insurance requirements.

Should You Put 20% Down?

A 20% down payment has long been considered a financial milestone because it reduces the amount borrowed and may eliminate private mortgage insurance on many conventional loans. However, waiting years to save 20% isn’t always the best decision for every buyer.

Many homeowners successfully purchase homes with smaller down payments and begin building equity sooner. The right amount depends on your income, savings, monthly budget, and long-term financial goals.

Comparing Different Down Payment Amounts

| Down Payment | Loan Amount | Monthly Payment |

|---|---|---|

| 5% | Higher | Higher |

| 10% | Moderate | Moderate |

| 20% | Lower | Lower |

This comparison illustrates why many buyers use a down payment calculator before choosing a mortgage. Even a small increase in your upfront payment can have a meaningful impact on your monthly housing costs.

Buying Land Instead of a Home

Some buyers purchase land before building a home. In these situations, financing works differently than a traditional mortgage.

If you’re comparing financing options for undeveloped property, you may also want to use a land loan calculator with down payment. Land loans often have different qualification requirements, interest rates, and down payment expectations than standard home mortgages.

Plan Your Home Purchase with Confidence

Knowing your expected down payment before shopping for a home can help you create a realistic budget and avoid surprises during the mortgage process.

By adjusting different purchase prices and down payment amounts, you can compare multiple financing scenarios and determine which option best fits your financial goals.

Frequently Asked Questions

A down payment calculator estimates how much money you’ll need to pay upfront when purchasing a home and shows how your down payment affects the amount you need to borrow.

The amount depends on the type of mortgage, lender requirements, and your financial situation. While some buyers choose to put down 20%, many loan programs allow qualified borrowers to purchase a home with a smaller down payment.

The minimum down payment varies depending on the mortgage program. Government-backed loans and conventional mortgages often have different eligibility requirements and minimum down payment guidelines.

Yes. A larger down payment reduces your loan amount, which generally results in a lower monthly mortgage payment and less interest paid over the life of the loan.

Not necessarily. While a larger down payment offers financial advantages, many buyers choose to purchase a home sooner with a smaller down payment if it fits their budget and long-term goals.

Yes. The calculator can help estimate the required down payment for many types of residential real estate purchases, although lender requirements may differ for investment properties.

Yes. While this calculator provides general estimates, buyers financing undeveloped land may also benefit from using a dedicated land loan calculator with down payment because land loans often have different lending requirements.

Your down payment affects your loan amount, monthly payment, borrowing costs, home equity, and whether mortgage insurance may be required. Understanding these factors helps you make more informed home-buying decisions.