Our HELOC Calculator helps you estimate how much you may be able to borrow using the equity in your home, calculate potential monthly payments, and better understand the costs of a Home Equity Line of Credit (HELOC). Whether you're planning a home renovation, consolidating high-interest debt, or preparing for a major expense, this calculator provides a practical starting point for evaluating your borrowing options.

Unlike a traditional mortgage or home equity loan, a HELOC works as a revolving line of credit. You can borrow money as needed during the draw period, repay what you use, and often borrow again until the credit line expires. Because interest is charged only on the outstanding balance, many homeowners use a HELOC as a flexible financing solution rather than borrowing one large lump sum.

What Is a HELOC?

A Home Equity Line of Credit (HELOC) is a revolving credit line secured by the equity you've built in your home. Equity is generally the difference between your home's current market value and the remaining balance on your mortgage.

Rather than receiving all of the money upfront, a HELOC allows you to withdraw funds as needed, up to your approved credit limit, during a specified draw period. Once that period ends, you'll typically enter the repayment period, when no additional borrowing is allowed and the outstanding balance must be repaid.

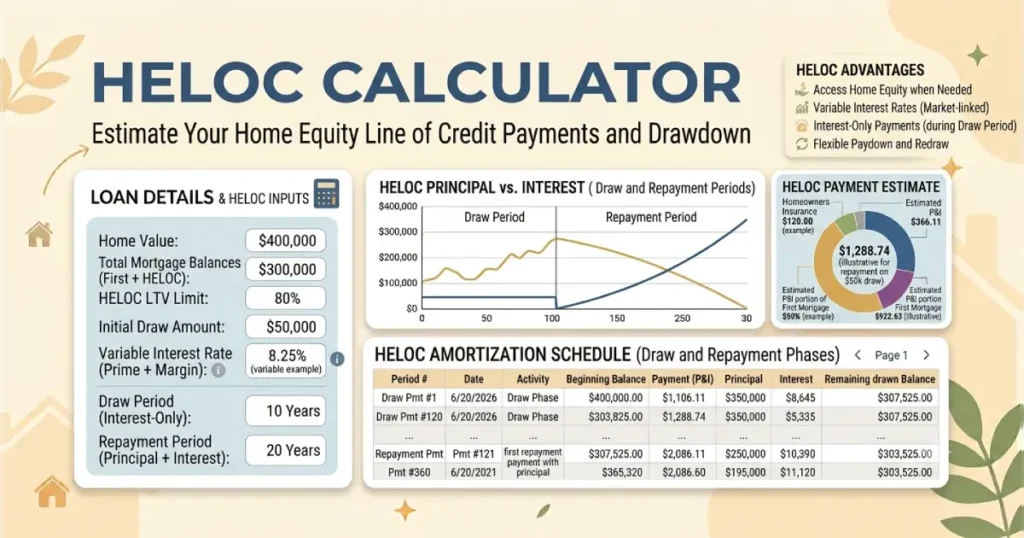

How the HELOC Calculator Works

Our calculator estimates your available borrowing amount and monthly payment based on your home's value, your existing mortgage balance, interest rate, and repayment period.

To get started, enter:

- Current home value

- Remaining mortgage balance

- Desired HELOC amount

- Interest rate

- Draw period (if applicable)

- Repayment period

The calculator then estimates your available home equity, your potential borrowing limit, estimated monthly payments, and the total interest paid based on the information you provide.

How Home Equity Is Calculated

Your available equity is generally calculated by subtracting your remaining mortgage balance from your home's estimated market value.

For example, if your home is worth $500,000 and you still owe $300,000 on your mortgage, you have approximately $200,000 in home equity. However, lenders typically allow borrowers to access only a portion of that equity rather than the full amount.

The exact borrowing limit depends on the lender's loan-to-value (LTV) requirements, your credit profile, income, and other underwriting factors.

How HELOC Interest Works

Most HELOCs have variable interest rates, meaning your interest rate may increase or decrease over time based on changes in the market. As a result, your monthly payment may also change throughout the life of the credit line.

During the draw period, many borrowers are required to make interest-only payments, although some lenders also allow principal payments. Once the repayment period begins, monthly payments generally increase because both principal and interest must be repaid.

Common Uses for a HELOC

- Home remodeling and renovation projects.

- Debt consolidation.

- Education expenses.

- Emergency financial needs.

- Major home repairs.

- Medical expenses.

- Business or investment opportunities.

Because your home serves as collateral, it's important to borrow responsibly and ensure the loan fits comfortably within your long-term budget.

HELOC vs. Home Equity Loan

| Feature | HELOC | Home Equity Loan |

|---|---|---|

| Funds | Borrow as needed | Single lump sum |

| Interest Rate | Usually variable | Often fixed |

| Payments | Can vary | Usually fixed |

| Best For | Ongoing expenses | One-time projects |

Choosing between a HELOC and a home equity loan depends on how you plan to use the funds and whether you prefer flexible borrowing or predictable monthly payments.

What Affects Your HELOC Payment?

Several factors influence your monthly payment and the total cost of borrowing.

- Your outstanding HELOC balance.

- Your interest rate.

- Changes in variable interest rates.

- The length of the draw period.

- Your repayment term.

- Whether you're making interest-only or principal-and-interest payments.

Running different scenarios through the calculator can help you estimate how changing interest rates or borrowing amounts may affect your future payments.

Should You Use a HELOC?

A HELOC may be a suitable financing option for homeowners who need flexibility and plan to borrow money gradually rather than all at once. However, because your home secures the line of credit, missed payments could increase your financial risk.

Before opening a HELOC, compare interest rates, fees, repayment terms, and your ability to comfortably manage future payments if variable rates increase.

Frequently Asked Questions

A HELOC calculator estimates how much you may be able to borrow based on your available home equity and helps estimate monthly payments and borrowing costs.

The amount depends on your home's value, your remaining mortgage balance, your lender's loan-to-value limits, your credit history, income, and other qualification requirements.

Home equity is generally calculated by subtracting your remaining mortgage balance from your home's current market value.

Many HELOCs have variable interest rates that may increase or decrease over time. As rates change, your monthly payment may also change.

A HELOC functions like a revolving line of credit that allows you to borrow funds as needed, while a home equity loan provides a single lump-sum payment with scheduled repayment.

Yes. Home renovations are one of the most common reasons homeowners use a HELOC because funds can be accessed as projects progress.

Once the draw period expires, you typically enter the repayment period, during which you can no longer borrow additional funds and must repay the outstanding balance according to your loan agreement.

This calculator provides estimates based on the information you enter. Your actual borrowing limit, interest rate, monthly payment, and loan terms will depend on your lender's underwriting guidelines and current market conditions.