Buying a home is one of the most significant financial milestones in life. However, before you start browsing real estate listings, the absolute first question you need to answer is: “How much house can I afford?”

Falling in love with a home that stretches your budget too thin can lead to financial stress, a phenomenon known as being “house poor.” To help you make a smart, sustainable decision, this guide breaks down the golden rules of home affordability, the hidden costs of homeownership, and how lenders evaluate your income.

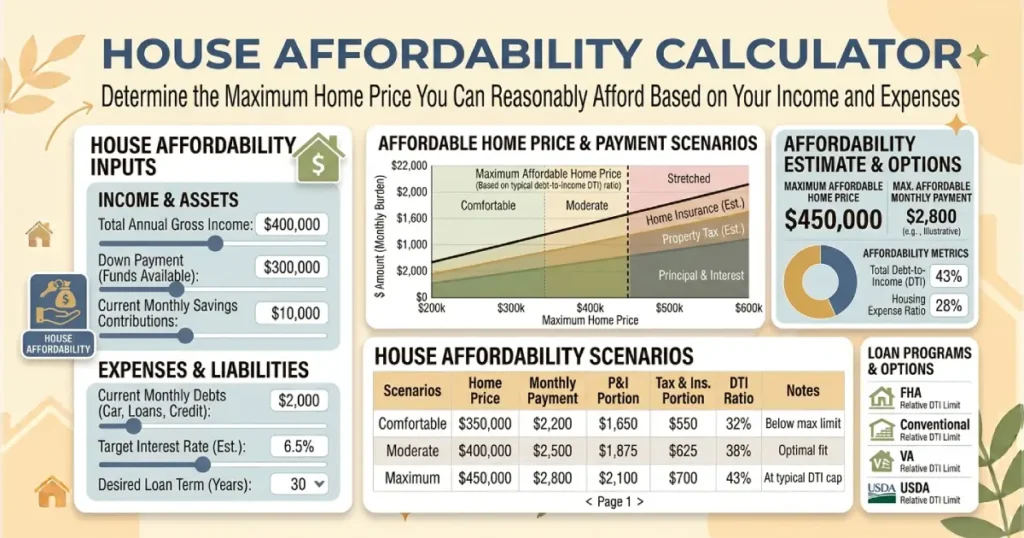

Ready to test your own numbers? You can instantly calculate your personalized budget using this intuitive House Affordability Calculator.

The Golden Rules of Home Affordability

Financial experts and mortgage lenders use a few baseline ratios to determine a safe housing budget. While every financial situation is unique, these three rules provide a solid foundation.

1. The 28/36 Rule

This is the standard benchmark used by most traditional lenders:

- The 28% Front-End Ratio: Your total monthly housing costs (including mortgage principal, interest, taxes, and insurance) should not exceed 28% of your gross monthly income (before taxes).

- The 36% Back-End Ratio: Your total monthly debt payments (housing costs plus student loans, car payments, credit cards, and child support) should not exceed 36% of your gross monthly income.

2. The 35/43 Rule

Some flexible mortgage programs allow for slightly higher limits:

- Your total monthly housing costs should not exceed 35% of your gross income.

- Your total debt payments should not exceed 43% of your gross income. This 43% mark is often the maximum debt-to-income ratio allowed for a qualified mortgage.

3. The 25% Post-Tax (Net) Rule

If you prefer a more conservative approach, many financial planners suggest keeping your housing expenses under 25% of your net (take-home) pay after taxes. This ensures you still have plenty of breathing room for retirement savings, travel, and lifestyle expenses.

Key Factors That Determine Your Home Budget

Lenders do not just look at your salary; they evaluate your entire financial profile. Here are the four critical pillars of home affordability:

- Gross Monthly Income: Your steady income before taxes. This includes base salary, reliable bonuses, and documented secondary income.

- Debt-to-Income (DTI) Ratio: The percentage of your gross monthly income that goes toward paying recurring debts. A lower DTI makes you a more attractive borrower and qualifies you for better interest rates.

- Down Payment: The cash you put down upfront. While a 20% down payment is ideal to avoid paying Private Mortgage Insurance (PMI), many loans allow as little as 3% to 5% down.

- Credit Score: Your credit score directly impacts your interest rate. A higher score means a lower interest rate, which slashes your monthly mortgage payment and increases your total buying power.

Don’t Forget the Hidden Costs of Homeownership

When calculating how much house you can afford, looking only at the mortgage principal and interest is a common trap. A true budget must account for PITI and ongoing maintenance:

- Principal: The actual money going toward paying down the loan balance.

- Interest: The cost of borrowing the money from the lender.

- Taxes: Property taxes vary heavily by location and can add hundreds of dollars to your monthly payment.

- Insurance: Homeowners insurance is required by lenders to protect the asset.

- HOA Fees: If you buy a condo or a home in a planned community, Homeowners Association fees are a non-negotiable monthly expense.

- Maintenance Fund: As a homeowner, you are the landlord. Experts recommend setting aside 1% to 2% of the home’s total value annually for unexpected repairs (e.g., roofing, HVAC, plumbing).

To see how these variables interact and impact your actual monthly cash flow, plug your estimated numbers into the House Affordability Calculator.

Frequently Asked Questions

For a conventional mortgage, lenders generally look for a DTI ratio of 36% or lower. However, depending on your credit score and down payment size, some lenders will approve a DTI up to 43%, and certain government-backed loans (like FHA loans) may go even higher under specific compensating factors.

Yes. Many conventional loan programs tailored for first-time homebuyers allow down payments as low as 3%. Additionally, FHA loans require a minimum of 3.5%, and VA or USDA loans offer 0% down options for qualified borrowers. Keep in mind that putting down less than 20% will usually require you to pay Private Mortgage Insurance (PMI).

Your credit score dictates your mortgage interest rate. A lower interest rate means you pay less money toward interest each month, which gives you more borrowing power to put toward the actual price of the home. Moving from a “fair” credit score to an “excellent” score can save you tens of thousands of dollars over the life of a 30-year loan.

Pre-qualification is a quick, informal estimate of what you might be able to borrow based on self-reported financial data. Pre-approval is a formal process where a lender verifies your financial documents (tax returns, pay stubs, credit history) and gives you a written commitment for a specific loan amount. Pre-approval is much stronger when making an offer on a home.

Being house poor describes a situation where a homeowner spends such a large percentage of their total monthly income on housing expenses (mortgage, taxes, utilities, maintenance) that they have very little cash left over for other necessities, savings, emergencies, or discretionary spending.

It is highly recommended to keep an emergency fund equal to 3 to 6 months of living expenses completely separate from your down payment and closing costs. Buying a home involves upfront expenses like moving costs, immediate repairs, and furnishing, so draining your entire savings for the down payment leaves you financially vulnerable.